"Data-Driven Optimization in Pricing and Revenue Management" by Arnoud den Boer - Lecture 1

In this course we will study data-driven decision problems: optimization problems for which the relation between decision and outcome is unknown upfront, and thus has to be learned on-the-fly from accumulating data. This type of problems has an intrinsic tension between statistical goals a

From playlist Thematic Program on Stochastic Modeling: A Focus on Pricing & Revenue Management

Basic stochastic simulation b: Stochastic simulation algorithm

(C) 2012-2013 David Liao (lookatphysics.com) CC-BY-SA Specify system Determine duration until next event Exponentially distributed waiting times Determine what kind of reaction next event will be For more information, please search the internet for "stochastic simulation algorithm" or "kin

From playlist Probability, statistics, and stochastic processes

Introduction to the paper https://arxiv.org/abs/2002.06707

From playlist Research

“Data-Driven Pricing” – Prof. Omar Besbes

Pricing is central to many industries and academic disciplines ranging from Operations Research to Economics and Computer Science. At the heart of pricing lies a fundamental informational dimension regarding the level of knowledge about customers' values. In practice, the latter comes from

From playlist Thematic Program on Stochastic Modeling: A Focus on Pricing & Revenue Management

"Diffusion Approximation and Sequential Experimentation" by Victor Araman

We consider a Bayesian sequential experimentation problem. We identify environments in which the average number of experiments that is conducted per unit of time is large and the informativeness of each individual experiment is low. Under such regimes, we derive a diffusion approximation f

From playlist Thematic Program on Stochastic Modeling: A Focus on Pricing & Revenue Management

"Data-Driven Optimization in Pricing and Revenue Management" by Arnoud den Boer - Lecture 3

In this course we will study data-driven decision problems: optimization problems for which the relation between decision and outcome is unknown upfront, and thus has to be learned on-the-fly from accumulating data. This type of problems has an intrinsic tension between statistical goals a

From playlist Thematic Program on Stochastic Modeling: A Focus on Pricing & Revenue Management

"Data-Driven Optimization in Pricing and Revenue Management" by Arnoud den Boer - Lecture 2

In this course we will study data-driven decision problems: optimization problems for which the relation between decision and outcome is unknown upfront, and thus has to be learned on-the-fly from accumulating data. This type of problems has an intrinsic tension between statistical goals a

From playlist Thematic Program on Stochastic Modeling: A Focus on Pricing & Revenue Management

An introduction to multilevel Monte Carlo methods – Michael Giles – ICM2018

Numerical Analysis and Scientific Computing Invited Lecture 15.7 An introduction to multilevel Monte Carlo methods Michael Giles Abstract: In recent years there has been very substantial growth in stochastic modelling in many application areas, and this has led to much greater use of Mon

From playlist Numerical Analysis and Scientific Computing

Paolo Guasoni, Lesson II - 19 december 2017

QUANTITATIVE FINANCE SEMINARS @ SNS PROF. PAOLO GUASONI TOPICS IN PORTFOLIO CHOICE

From playlist Quantitative Finance Seminar @ SNS

Paolo Guasoni, Lesson I - 18 december 2017

QUANTITATIVE FINANCE SEMINARS @ SNS PROF. PAOLO GUASONI TOPICS IN PORTFOLIO CHOICE

From playlist Quantitative Finance Seminar @ SNS

Fifteenth SIAM Activity Group on FME Virtual Talk

Date: Thursday, December 10, 1PM-2PM Early Career Talks Speaker 1: Dena Firoozi, HEC Montréal - University of Montreal Title: Belief Estimation by Agents in Major-Minor LQG Mean Field Games Speaker 2: Sveinn Olafsson, Columbia University Title: Personalized Robo-Advising: Enhancing Inves

From playlist SIAM Activity Group on FME Virtual Talk Series

Paolo Guasoni, Lesson III - 20 december 2017

QUANTITATIVE FINANCE SEMINARS @ SNS PROF. PAOLO GUASONI TOPICS IN PORTFOLIO CHOICE

From playlist Quantitative Finance Seminar @ SNS

[T1 2022] Sebastian Schreiber - Coevolution of habitat choice in a stochastic world

Joint work with Alex Hening and Dang Nguyen. Species live and interact in patchy landscapes where environmental conditions vary both in time and space. In the face of this spatial-temporal heterogeneity, species may co-evolve how they select habitat patches. Under equilibrium conditions,

From playlist [T1 2022] Workshop - Mathematical models in ecology and evolution - March 21st to 25th, 2022

Fourteenth SIAM Activity Group on FME Virtual Talk

Speakers: Damir Filipovic, EPFL and Swiss Finance Institute Title: A Machine Learning Approach to Portfolio Pricing and Risk Management for High-Dimensional Problems Moderator: Rene Carmona, Princeton University

From playlist SIAM Activity Group on FME Virtual Talk Series

The coordination of centralised and distributed generation - René Aid, Univeristé Paris-Dauphine PSL

This workshop is kindly sponsored by London Mathematical Society, EPSRC and is part of the Lloyd's Register Foundation programme on Data-centric engineering at The Alan Turing Institute. The workshop "Mean-field games, energy and environment" aims to bring together leading experts in the f

From playlist Mean-field games, energy and environment

Elias Khalil - Neur2SP: Neural Two-Stage Stochastic Programming - IPAM at UCLA

Recorded 02 March 2023. Elias Khalil of the University of Toronto presents "Neur2SP: Neural Two-Stage Stochastic Programming" at IPAM's Artificial Intelligence and Discrete Optimization Workshop. Abstract: Stochastic Programming is a powerful modeling framework for decision-making under un

From playlist 2023 Artificial Intelligence and Discrete Optimization

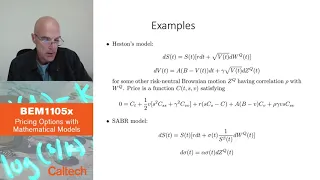

8 2 Stochastic Volatility Part 2

BEM1105x Course Playlist - https://www.youtube.com/playlist?list=PL8_xPU5epJdfCxbRzxuchTfgOH1I2Ibht Produced in association with Caltech Academic Media Technologies. ©2020 California Institute of Technology

From playlist BEM1105x Course - Prof. Jakša Cvitanić

Dr Lukasz Szpruch, University of Edinburgh

Bio I am a Lecturer at the School of Mathematics, University of Edinburgh. Before moving to Scotland I was a Nomura Junior Research Fellow at the Institute of Mathematics, University of Oxford, and a member of Oxford-Man Institute for Quantitative Finance. I hold a Ph.D. in mathematics fr

From playlist Short Talks

6 1 Black Scholes Merton pricing Part 1

BEM1105x Course Playlist - https://www.youtube.com/playlist?list=PL8_xPU5epJdfCxbRzxuchTfgOH1I2Ibht Produced in association with Caltech Academic Media Technologies. ©2020 California Institute of Technology

From playlist BEM1105x Course - Prof. Jakša Cvitanić