Model Theory - part 01 - The Setup in Classical Set Valued Model Theory

Here we give the basic setup for Model Theory. I learned this from a talk Tom Scanlon gave in 2010 at CUNY.

From playlist Model Theory

The Atom A3 The Bohr Model of the Hydrogen Atom

The Bohr model of the atom.

From playlist Physics - The Atom

The Atom B1 The Quantum Mechanical Picture of the Atom

The quantum mechanical model of the atom.

From playlist Physics - The Atom

The Atom A4 The Bohr Model of the Hydrogen Atom

The Bohr model of the atom.

From playlist Physics - The Atom

The Atom A5 The Bohr Model of the Hydrogen Atom

The Bohr model of the atom.

From playlist Physics - The Atom

The Nuclear Shell Model: An Introduction

A basic introduction to the shell model to explain magic numbers in nuclei.

From playlist Nuclear Physics

Quantum Physics: Early Models of the Atom (and why they feel SO right... but aren't)

The Rutherford Planetary and Bohr models of the atom have certain very satisfying qualities to them. It's just a shame they're incorrect... Hey everyone, I'm back with another fun physics video. This time, I wanted to shed some light on a couple of models of the atom that existed around t

From playlist Quantum Physics by Parth G

Symmetry and Quantum Electrodynamics (The Standard Model Part 1)

The Standard Model of Particle Physics is an absolutely incredible theory and a triumph of modern physics capable of explaining almost all of the physical phenomena we observe in nature. However, to understand it, we need to dive into some deep ideas including symmetry and how these relate

From playlist Standard Model

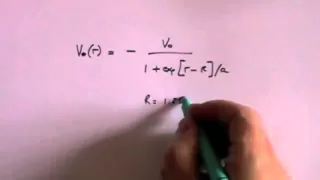

FRM: How d2 in Black-Scholes becomes PD in Merton model

In Black-Scholes, N(d2) is the probability that the option will be struck in the risk-neutral world. The Merton model for credit risk uses the Black-Scholes by treating equity as a call option on firm assets. In Merton, d2 becomes the "distance to default" and N(-d2) becomes the probabilit

From playlist Derivatives: Option Pricing

Fin Math L5-3: Towards Black-Scholes-Merton

Welcome to the last part of Lesson 5. In this video we cover some last relevant topics to finally deal with the Black-Scholes-Merton theorem, which will be the starting point of all our pricing exercises. Here you can download the new chapter of the lecture notes: https://www.dropbox.com/s

From playlist Financial Mathematics

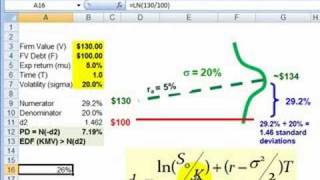

FRM: Expected default frequency (EDF, PD) with Merton Model

A visual and Excel-based review of the Merton model used to estimate EDF (or probability of default). This is a structural approach; i.e,. default is predicted by the firm's balance sheet properties. For more financial risk videos, visit our website! http://www.bionicturtle.com

From playlist Credit Risk: Introduction

The Black-Scholes-Merton Model | FRM Video Tutorials| FRM Certification and Training | Simplilearn

🔥 Explore More Courses By Simplilearn: https://www.simplilearn.com/?utm_campaign=TheBlackScholesMertonModelJen2-I74skraJ_Uo&utm_medium=DescriptionFirstFold&utm_source=youtube This video explains the: 1.Black-Scholes-Merton Model 2.Assumptions 3.Realized Return and Volatility 4.European Op

From playlist FRM Tutorial | Financial Risk Management Tutorial | Simplilearn

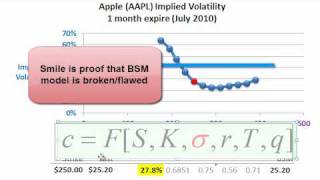

A plot of implied volatility (i.e., the volatility that forces the BSM model option price to equal the observed market price) against strike price. The smile is proof the model is imprecise (incorrect in some assumption); e.g., returns are not lognormally distributed. For more financial ri

From playlist Volatility

5 1 Brownian motion process Part 1

BEM1105x Course Playlist - https://www.youtube.com/playlist?list=PL8_xPU5epJdfCxbRzxuchTfgOH1I2Ibht Produced in association with Caltech Academic Media Technologies. ©2020 California Institute of Technology

From playlist BEM1105x Course - Prof. Jakša Cvitanić

Pricing Options using Black Scholes Merton

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle The Black–Scholes or Black–Scho

From playlist Class 3: Pricing Financial Options

The Part-Abandoned Tooting, Merton & Wimbledon Railway

You want abandoned railways? Here’s one. You want Thameslink? We got that too. Trams? Don’t even worry about it. https://ko-fi.com/jagohazzard https://www.patreon.com/jagohazzard

From playlist London

Exotic option: exchange option (FRM T3-47)

[my xls is here https://trtl.bz/2C9PEXC] Instead of a fixed exercise price, an exchange option has an exercise price linked to some other asset. In my illustrated example here, the exchange option holder will pay (as the exercise price) 80X the price of silver in exchange for receiving one

From playlist FM&P: Intro to Derivatives: Exotic options (FRM Topic 3)

The Atom B2 The Quantum Mechanical Picture of the Atom

The quantum mechanical model of the atom.

From playlist Physics - The Atom

Lognormal property of stock prices assumed by Black-Scholes (FRM T4-10)

Although the Black-Scholes option pricing model makes several assumptions, the most important is the first assumption that stock prices follow a lognormal distribution (and that volatility is constant). Specifically, the model assumes that log RETURNS (aka, continuously compounded returns)

From playlist Valuation and RIsk Models (FRM Topic 4)