What is Value at Risk? VaR and Risk Management

In todays video we learn about Value at Risk (VaR) and how is it calculated? Buy The Book Here: https://amzn.to/37HIdEB Follow Patrick on Twitter Here: https://twitter.com/PatrickEBoyle What Is Value at Risk (VaR)? Value at risk (VaR) is a calculation that aims to quantify the level of

From playlist Risk Management

Risk Management Lesson 5A: Value at Risk

In this first part of Lesson 5, we discuss Value-at-Risk (VaR). Topics: - Definition of VaR - Loss distribution and confidence level - The normal VaR

From playlist Risk Management

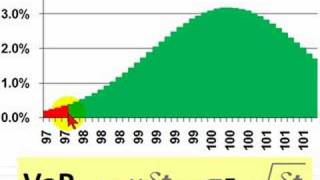

Marginal value at risk (marginal VaR)

This is a review which follows Jorion's (Chapter 7) calculation of marginal value at risk (marginal VaR). Marginal VaR requires that we calculate the beta of a position with respect to the portfolio. For more financial risk videos, visit our website! http://www.bionicturtle.com

From playlist Value at Risk (VaR): Introduction

FRM: Parametric value at risk (VaR): Pros & Cons

Here is a quick explanation of parametric value at risk (VaR) as a means to illustrating its strengths/weaknesses. Please note: The essence of parametric VaR is "no data:" while historical data is surely used to select a distribution and calibrate its parameters, a parametric VaR leans on

From playlist Value at Risk (VaR): Introduction

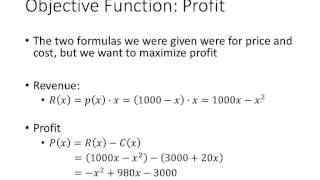

In this video, we go through an example of an application problem using price, revenue, and cost functions to maximize profit.

From playlist Calculus

QRM L1-1: The Definition of Risk

Welcome to Quantitative Risk Management (QRM). In this first class, we define what risk if for us. We will discuss the basic characteristics of risk, underlining some important facts, like its subjectivity, and the impossibility of separating payoffs and probabilities. Understanding the d

From playlist Quantitative Risk Management

FRM: Surplus at risk (Pension VaR)

Surplus as risk is value at risk (VaR) for a pension fund. For more financial risk videos, visit our website! http://www.bionicturtle.com

From playlist Value at Risk (VaR): Introduction

FRM: Three approaches to value at risk (VaR)

This is a brief introduction to the three basic approaches to value at risk (VaR): Historical simulation, Monte Carlo simulation, Parametric VaR (e.g., delta normal). For more financial risk videos, visit our website at http://www.bionicturtle.com!

From playlist Value at Risk (VaR): Introduction

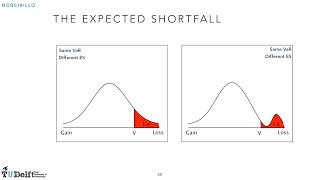

Risk Management 5B: Value at Risk (continued) and Expected Shortfall

This is the second part of Lesson 5. Topics: - The VaR for empirical distributions - The Expected Shortfall - Coherence of VaR and ES

From playlist Risk Management

FRM: Theory of normal backwardation

This is the classic, but difficult idea, that offers an explanation for why we expect the forward price to be less than the expected future spot price: F less than E[future spot]. The key to the theory is the assumption that hedgers are, on average, taking short positions (e.g., a corn fa

From playlist Derivatives: Commodity Futures

Frank H. Knight and Risk, Uncertainty and Profit - Prof. Ross Emmett

Speaker Ross Emmett, Professor of Economic Thought, School of Civic and Economic Thought and Leadership, and Director, Center for the Study of Economic Liberty, Arizona State University Abstract Frank Knight’s Risk, Uncertainty and Profit was published in 1921, and has remained in publi

From playlist Uncertainty and Risk

Business Analyst Interview Questions & Answers | Business Analyst Training For Beginners|Simplilearn

🔥Business Analyst Program (Discount Coupon: YTBE15) : https://www.simplilearn.com/business-analyst-certification-training-course ?utm_campaign=BusinessAnalystIQs&utm_medium=Descriptionff&utm_source=youtube 🔥 Professional Certificate Program In Business Analysis: https://www.simplilearn.com

From playlist Business Analyst Training Videos

Fixed income: Carry roll down (FRM T4-31)

Financial Risk Manager (FRM, Topic 4: Valuation and Risk Models, Fixed Income, Bruce Tuckman Chapter 3, Returns, Spreads and Yields). The Carry-Roll-Down is the price change in the bond due exclusively to the passage of time. It is only one component of a bond's total profit and loss (P&L)

From playlist Valuation and RIsk Models (FRM Topic 4)

How Do Stock Traders Profit When The Market Falls?

This video tutorial explains how traders profit when the stock market falls. This video discusses the concept of buying stocks vs short selling. It also covers option contracts such as buying and selling call and put options. It also discusses the maximum gain, risks, and potential retu

From playlist Stocks and Bonds

Valuation Modelling | Financial Modelling Training | Financial Modelling Tutorial | Simplilearn

🔥 Explore Best Courses By Simplilearn: https://www.simplilearn.com/?utm_campaign=ValuationModeling-y0t4uw0FWI4&utm_medium=DescriptionFirstFold&utm_source=youtube Basic valuation techniques are as follows 1. Past performance: Past performance informs us on the historical average level of t

From playlist Microsoft Excel Tutorial Videos 🔥[2022 Updated]

Applied Portfolio Management | Hedge Funds (Part 2) How Hedge Funds Invest | Trading Strategies

All slides are available on my Patreon page: https://www.patreon.com/PatrickBoyleOnFinance Applied Portfolio Management - How Hedge Funds Invest. Part Two In yesterdays class we learned what a hedge fund is, why people invest in them, and how hedge funds and other alternative investments

From playlist Applied Portfolio Management

10. Normative Frameworks for Business Decisions

MIT 15.031J Energy Decisions, Markets, and Policies, Spring 2012 View the complete course: http://ocw.mit.edu/15-031JS12 Instructor: Richard Schmalensee License: Creative Commons BY-NC-SA More information at http://ocw.mit.edu/terms More courses at http://ocw.mit.edu

From playlist MIT 15.031J Energy Decisions, Markets, Policies, Spring 2012

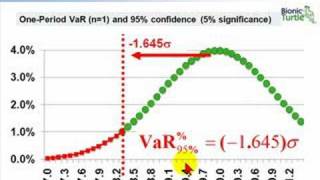

How do you calculate value at risk? Two ways of calculating VaR

In todays video we learn how to calculate VaR or Value at Risk. Buy The Book Here: https://amzn.to/37HIdEB Follow Patrick on Twitter Here: https://twitter.com/PatrickEBoyle What is VAR? The most popular and traditional measure of risk is volatility. The main problem with volatility, how

From playlist Risk Management