Marginal value at risk (marginal VaR)

This is a review which follows Jorion's (Chapter 7) calculation of marginal value at risk (marginal VaR). Marginal VaR requires that we calculate the beta of a position with respect to the portfolio. For more financial risk videos, visit our website! http://www.bionicturtle.com

From playlist Value at Risk (VaR): Introduction

Risk Management Lesson 5A: Value at Risk

In this first part of Lesson 5, we discuss Value-at-Risk (VaR). Topics: - Definition of VaR - Loss distribution and confidence level - The normal VaR

From playlist Risk Management

How much would it take for you to risk $10? Check out Audible: http://bit.ly/AudibleVe Can you solve this? http://bit.ly/248Ve Regression to the mean: http://bit.ly/VeRTTM Help translate Veritasium videos into other languages: http://veritasium.subtitl.us Psychological literature shows t

From playlist New Here? Try These!

What is Value at Risk? VaR and Risk Management

In todays video we learn about Value at Risk (VaR) and how is it calculated? Buy The Book Here: https://amzn.to/37HIdEB Follow Patrick on Twitter Here: https://twitter.com/PatrickEBoyle What Is Value at Risk (VaR)? Value at risk (VaR) is a calculation that aims to quantify the level of

From playlist Risk Management

QRM L1-1: The Definition of Risk

Welcome to Quantitative Risk Management (QRM). In this first class, we define what risk if for us. We will discuss the basic characteristics of risk, underlining some important facts, like its subjectivity, and the impossibility of separating payoffs and probabilities. Understanding the d

From playlist Quantitative Risk Management

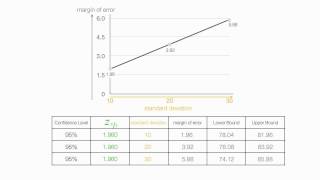

How to calculate margin of error and standard deviation

In this tutorial I show the relationship standard deviation and margin of error. I calculate margin of error and confidence intervals with different standard deviations. Playlist on Confidence Intervals http://www.youtube.com/course?list=EC36B51DB57E3A3E8E Like us on: http://www.facebook

From playlist Confidence Intervals

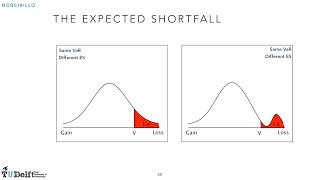

Risk Management 5B: Value at Risk (continued) and Expected Shortfall

This is the second part of Lesson 5. Topics: - The VaR for empirical distributions - The Expected Shortfall - Coherence of VaR and ES

From playlist Risk Management

How to calculate Margin of Error Confidence Interval for a population proportion

In this tutorial I explain and then calculate, using an example, the margin of error and confidence interval for a population proportion. Like us on: http://www.facebook.com/PartyMoreStudyLess Link To Playlist on Confidence Intervals http://www.youtube.com/course?list=EC36B51DB57E3A3E8E

From playlist Confidence Intervals

How do you calculate value at risk? Two ways of calculating VaR

In todays video we learn how to calculate VaR or Value at Risk. Buy The Book Here: https://amzn.to/37HIdEB Follow Patrick on Twitter Here: https://twitter.com/PatrickEBoyle What is VAR? The most popular and traditional measure of risk is volatility. The main problem with volatility, how

From playlist Risk Management

What is Futures Margin? - What Is It? How Does It Work?

What is Futures Margin? - What Is It? How Does It Work? These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://t

From playlist Class 1 Futures & Forwards

Margins, perceptrons, and deep networks - Matus Telgarsky

Seminar on Theoretical Machine Learning Topic: Margins, perceptrons, and deep networks Speaker: Matus Telgarsky-2020-03-26 Affiliation: University of Illinois Date: March 26, 2020 For more video please visit http://video.ias.edu

From playlist Mathematics

Twelfth SIAM Activity Group on FME Virtual Talk

Speakers: Michael J. Fleming, Federal Reserve Bank of New York Wenqian Huang, Bank of International Settlements David Rios, Columbia University and New York University Title: Implication of COVID 19 for Financial Markets Abstract: Dr. Fleming will discuss the pandemic's effect on the Tre

From playlist SIAM Activity Group on FME Virtual Talk Series

FRM: Why a futures price differs from a forward price

Why would the prices differ? The key difference is the daily settlement of the futures contract. The investor in a futures contract must maintain a margin account. The key issue is the correlation between the spot price and the interest rate. If the correlation (spot, interest rate) is str

From playlist Derivatives: Interest Rate Derivatives

Dependence Uncertainty and Risk - Prof. Paul Embrechts

Abstract I will frame this talk in the context of what I refer to as the First and Second Fundamental Theorem of Quantitative Risk Management (1&2-FTQRM). An alternative subtitle for 1-FTQRM would be "Mathematical Utopia", for 2-FTQRM it would be "Wall Street Reality". I will mainly conce

From playlist Uncertainty and Risk

MIT 14.01 Principles of Microeconomics, Fall 2018 Instructor: Prof. Jonathan Gruber View the complete course: https://ocw.mit.edu/14-01F18 YouTube Playlist: https://www.youtube.com/playlist?list=PLUl4u3cNGP62oJSoqb4Rf-vZMGUBe59G- This video explains the economic concept of decision making

From playlist MIT 14.01 Principles of Microeconomics, Fall 2018

MIT 14.13 Psychology and Economics, Spring 2020 Instructor: Prof. Frank Schilbach View the complete course: https://ocw.mit.edu/14-13S20 YouTube Playlist: https://www.youtube.com/playlist?list=PLUl4u3cNGP63Z979ri_UXXk_1zrvrF77Q In this video, Prof. Schilbach describes how economics looks

From playlist MIT 14.13 Psychology and Economics, Spring 2020

The benefits of a centralised margin infrastructure

David Maloy, COO of NetOTC, speaks to PwC Partner, Chris Matten about how NetOTC has been affected by centralised margin infrastructure at Risk Minds International 2015 in Amsterdam. Twitter: www.twitter.com/RiskMinds Linked In: www.linkedin.com/groups/3263290 Facebook: www.facebook.com/R

From playlist RiskMinds Live 2015

Introduction to Derivatives - Futures & Forwards - Revision Class1

A revision slideshow on Futures and Forwards. These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com

From playlist Revision Lectures

FRM: Parametric value at risk (VaR): Pros & Cons

Here is a quick explanation of parametric value at risk (VaR) as a means to illustrating its strengths/weaknesses. Please note: The essence of parametric VaR is "no data:" while historical data is surely used to select a distribution and calibrate its parameters, a parametric VaR leans on

From playlist Value at Risk (VaR): Introduction