Reference rates | Interest rates

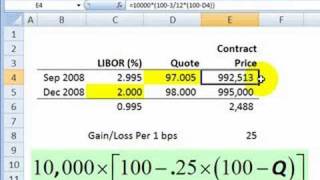

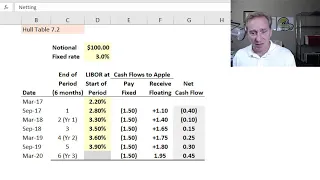

Libor

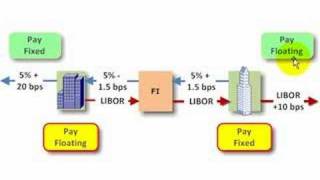

The London Inter-Bank Offered Rate is an interest-rate average calculated from estimates submitted by the leading banks in London. Each bank estimates what it would be charged were it to borrow from other banks. The resulting average rate is usually abbreviated to Libor (/ˈlaɪbɔːr/) or LIBOR, or more officially to ICE LIBOR (for Intercontinental Exchange LIBOR). It was formerly known as BBA Libor (for British Bankers' Association Libor or the trademark bba libor) before the responsibility for the administration was transferred to Intercontinental Exchange. It is the primary benchmark, along with the Euribor, for short-term interest rates around the world. Libor was phased out at the end of 2021, and market participants are being encouraged to transition to risk-free interest rates. As of late 2022, parts of it have been discontinued, and the rest is scheduled to end within 2023; the Secured Overnight Financing Rate (SOFR) is its replacement. Libor rates are calculated for five currencies and seven borrowing periods ranging from overnight to one year and are published each business day by Thomson Reuters. Many financial institutions, mortgage lenders, and credit card agencies set their own rates relative to it. At least $350 trillion in derivatives and other financial products are tied to Libor. In June 2012, multiple criminal settlements by Barclays Bank revealed significant fraud and collusion by member banks connected to the rate submissions, leading to the Libor scandal. The British Bankers' Association said on 25 September 2012 that it would transfer oversight of Libor to UK regulators, as proposed by Financial Services Authority managing director Martin Wheatley's independent review recommendations. Wheatley's review recommended that banks submitting rates to Libor must base them on actual inter-bank deposit market transactions and keep records of those transactions, that individual banks' Libor submissions be published after three months, and recommended criminal sanctions specifically for manipulation of benchmark interest rates. Financial institution customers may experience higher and more volatile borrowing and hedging costs after implementation of the recommended reforms. The UK government agreed to accept all of the Wheatley Review's recommendations and press for legislation implementing them. Significant reforms, in line with the Wheatley Review, came into effect in 2013 and a new administrator took over in early 2014. The British government regulates Libor through criminal and regulatory laws passed by Parliament. In particular, the Financial Services Act 2012 brings Libor under UK regulatory oversight and creates a criminal offence for knowingly or deliberately making false or misleading statements relating to benchmark-setting. (Wikipedia).