QRM L1-1: The Definition of Risk

Welcome to Quantitative Risk Management (QRM). In this first class, we define what risk if for us. We will discuss the basic characteristics of risk, underlining some important facts, like its subjectivity, and the impossibility of separating payoffs and probabilities. Understanding the d

From playlist Quantitative Risk Management

A review of the method used in the first building block of CreditMetrics, a ratings-based credit risk portfolio model. You can find the spreadsheet here: http://trtl.bz/2si88RS. For more financial risk videos, visit our website! http://www.bionicturtle.com

From playlist Credit Risk: Portfolio Risk

Risk Management Lesson 5A: Value at Risk

In this first part of Lesson 5, we discuss Value-at-Risk (VaR). Topics: - Definition of VaR - Loss distribution and confidence level - The normal VaR

From playlist Risk Management

What is financial risk? FRM Foundations (T1-01)

Financial risk includes market risk, credit risk, operational risk, liquidity risk, and investment risk. 💡 Discuss this video here in our FRM forum: https://trtl.bz/2ywkLLE 👉 Subscribe here https://www.youtube.com/c/bionicturtl... to be notified of future tutorials on expert finance and

From playlist Risk Foundations (FRM Topic 1)

What is Value at Risk? VaR and Risk Management

In todays video we learn about Value at Risk (VaR) and how is it calculated? Buy The Book Here: https://amzn.to/37HIdEB Follow Patrick on Twitter Here: https://twitter.com/PatrickEBoyle What Is Value at Risk (VaR)? Value at risk (VaR) is a calculation that aims to quantify the level of

From playlist Risk Management

Keith Garbutt: The future of sophisticated modelling development

At RiskMinds International, Liz MacKean interviews Keith Garbutt, Head of Risk Model Validation at Credit Suisse. He discusses how financial institutions are dealing with increasing regulatory requirements, and the cost implications of model validation for banks. Find out more at https://g

From playlist RiskMinds 2016

Intoduction to Financial Modeling | Financial Modeling Tutorial | What is Financial Modeling

This Financial Modeling tutorial helps you to learn financial modeling with examples. This video is ideal for beginners to learn the basics of financial modeling. To attend a live session, click here: http://goo.gl/0vZIOF This video helps you learn: • Why Financial Modeling ? • Cours

From playlist Financial Modeling Tutorial Videos

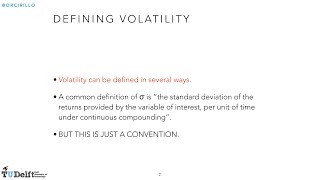

Risk Management Lesson 4A: Volatility

First part of Lesson 4. Topics: - Definitions of volatility - Basic assumptions (do they hold?) - Arch and G-arch models (brief overview)

From playlist Risk Management

Getting Started with Financial Modeling | Financial Modeling Tutorial | What is Financial Modeling

This Financial Modeling tutorial helps you to learn financial modeling with examples. This video is ideal for beginners to learn the basics of financial modeling. To attend a live session, click here: http://goo.gl/1fclPr This video helps you learn: • Why Financial Modeling ? • Cours

From playlist Financial Modeling Tutorial Videos

Climate risk management: What will regulatory developments mean for risk managers?

Financial institutions are preparing for a new dimension of risk management - climate risk. With new regulatory developments from the Biden administration and each of the 6 major US banks having made public net zero commitments, what will that mean for risk managers? PwC’s climate risk s

From playlist Webinars: At home with the experts

IMS Public Lecture: Mathematics and the Financial Crisis

Paul Embrechts, Swiss Federal Institute of Technology (ETH), Zurich

From playlist Public Lectures

Coronavirus: stress testing is about to get serious

As the COVID-19 curve is flattening, we are now eager to see what the post-pandemic landscape will look like after the dust is settled. With a wide range of medium-term economic outlooks out there, macro-economic scenario modelling will gain importance as a management tool since business p

From playlist Webinars: At home with the experts

Elimination of systamic risk in financial markets by Stefan Thurner

Program Summer Research Program on Dynamics of Complex Systems ORGANIZERS: Amit Apte, Soumitro Banerjee, Pranay Goel, Partha Guha, Neelima Gupte, Govindan Rangarajan and Somdatta Sinha DATE : 15 May 2019 to 12 July 2019 VENUE : Madhava hall for Summer School & Ramanujan hall f

From playlist Summer Research Program On Dynamics Of Complex Systems 2019

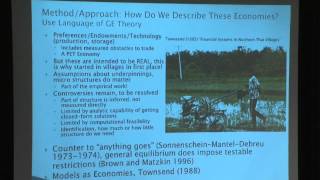

1. Finance, Growth, and Volatility

MIT 14.772 Development Economics: Macroeconomics, Spring 2013 View the complete course: http://ocw.mit.edu/14-772S13 Instructor: Robert Townsend Prof. Townsend introduces the course to the students, explains the syllabus, and covers the topics of finance, growth, and volatility. Chapters

From playlist MIT 14.772 Development Economics: Macroeconomics, Spring 2013

Webinar: Risk Transformation Agenda

Last year, PwC introduced our market study on how Global banks were looking to transform Risk functions in light of changing risk landscape, evolving business environment and focus on costs. Despite increasing consensus across Risk leadership on the need for change, there continue to be si

From playlist Webinars: At home with the experts

The Great Recession | International Economic Institutions | The Great Courses

The Great Recession was like a liquor tumbler of misused financial tools, misapplied risk models, interest rate mistakes, and bad government guidance on credit policy—and we all got dragged to the bar for shots. Line up for a hotly-debated risk management question of the tool versus its us

From playlist Latest Uploads

Quantitative Finance: Toward A General Framework for Modelling Roll-Over Risk

SIAM Activity Group on FME Virtual Talk Series Join us for a series of online talks on topics related to mathematical finance and engineering and running every two weeks until further notice. The series is organized by the SIAM Activity Group on Financial Mathematics and Engineering. Spea

From playlist SIAM Activity Group on FME Virtual Talk Series

Stock Market Predictions : Python for Finance 10

In previous videos we made a wonderful investment portfolio and now we will use regression analysis to make stock market predictions about the future performance of our portfolio. I’ll be using the ARIMA model for making stock market predictions in this video. It focuses on trying to fit

From playlist Python for Finance

Stanford Seminar - Entrepreneurial Thought Leaders: Hemant Shah of Risk Management Solutions

Hemant Shah Risk Management Solutions In this seminar, entrepreneurial leaders share lessons from real-world experiences across entrepreneurial settings. Speakers include entrepreneurs, leaders from global technology companies, venture capitalists, and best-selling authors. Half-hour talk

From playlist MS&E472 - Entrepreneurial Thought Leaders - Stanford Seminars