QRM 10-3: The Model Building Approach

This video is taken from by basic RM course and deals with MR under the model-building approach.

From playlist Quantitative Risk Management

(ML 11.3) Frequentist risk, Bayesian expected loss, and Bayes risk

A simple way to visualize the relationships between the frequentist risk, Bayesian expected loss, and Bayes risk.

From playlist Machine Learning

Risk Management Lesson 9B: Model-Building Approach to Market Risk

The second part of Lesson 9 still deals with Market Risk, but we discuss the model-building approach, in which we assume a model for our market variables. In particular we consider the so-called Var-Cov approach, which strongly relies on normality (a definitely unrealistic assumption, yet.

From playlist Risk Management

QRM L1-1: The Definition of Risk

Welcome to Quantitative Risk Management (QRM). In this first class, we define what risk if for us. We will discuss the basic characteristics of risk, underlining some important facts, like its subjectivity, and the impossibility of separating payoffs and probabilities. Understanding the d

From playlist Quantitative Risk Management

QRM 10-4: Model-Building with R Studio

In this video we give a simple example of model-building approach using R. The R studio file is available here: https://www.dropbox.com/s/gb58wm0jfxnl84f/Lesson10_2020.Rmd The data set here: https://www.dropbox.com/s/he1gidlcm9cxgig/historical.csv Enjoy!

From playlist Quantitative Risk Management

Risk Management Lesson 10: Operational Risk

In this last lesson, we deal with Operational Risk, a very important risk for banks. Unfortunately, its treatment in the Basel framework is not at all satisfactory. We will see why. Topics: - Definition of Operational Risk - Characteristics of Operational Risk - Basic Indicator Approach -

From playlist Risk Management

What is Value at Risk? VaR and Risk Management

In todays video we learn about Value at Risk (VaR) and how is it calculated? Buy The Book Here: https://amzn.to/37HIdEB Follow Patrick on Twitter Here: https://twitter.com/PatrickEBoyle What Is Value at Risk (VaR)? Value at risk (VaR) is a calculation that aims to quantify the level of

From playlist Risk Management

From playlist STAT 501

Risk Management Lesson 4A: Volatility

First part of Lesson 4. Topics: - Definitions of volatility - Basic assumptions (do they hold?) - Arch and G-arch models (brief overview)

From playlist Risk Management

Darwinian Model Risk and Reverse Stress Testing

SIAM Activity Group on FME Virtual Talk Series Join us for a series of online talks on topics related to mathematical finance and engineering and running every two weeks until further notice. The series is organized by the SIAM Activity Group on Financial Mathematics and Engineering. Dat

From playlist SIAM Activity Group on FME Virtual Talk Series

Stephan Wiehler: Minimum capital requirements for market risk under FRTB

A live recording of Stephan Wiehler, Head Rating Models and Stress Testing, Credit Suisse at RiskMinds International 2016. Find out more at https://goo.gl/KVtbtC.

From playlist RiskMinds Live 2016

Transfer Learning From Existing Diseases Via Hierarchical Multi-Modal BERT Models to Predict COVID19

Presented by: Khushbu Agarwal - Senior Research Scientist at Pacific Northwest National Laboratory Developing prediction models for emerging infectious diseases from relatively small numbers of cases is a critical need for improving pandemic preparedness. Using COVID-19 as an exemplar, we

From playlist Healthcare NLP Summit 2022

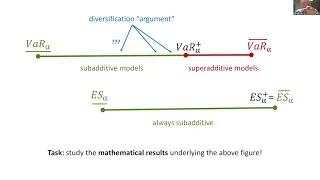

Dependence Uncertainty and Risk - Prof. Paul Embrechts

Abstract I will frame this talk in the context of what I refer to as the First and Second Fundamental Theorem of Quantitative Risk Management (1&2-FTQRM). An alternative subtitle for 1-FTQRM would be "Mathematical Utopia", for 2-FTQRM it would be "Wall Street Reality". I will mainly conce

From playlist Uncertainty and Risk

Webinar: Risk Transformation Agenda

Last year, PwC introduced our market study on how Global banks were looking to transform Risk functions in light of changing risk landscape, evolving business environment and focus on costs. Despite increasing consensus across Risk leadership on the need for change, there continue to be si

From playlist Webinars: At home with the experts

Keith Garbutt: The future of sophisticated modelling development

At RiskMinds International, Liz MacKean interviews Keith Garbutt, Head of Risk Model Validation at Credit Suisse. He discusses how financial institutions are dealing with increasing regulatory requirements, and the cost implications of model validation for banks. Find out more at https://g

From playlist RiskMinds 2016

Quantitative Finance: Toward A General Framework for Modelling Roll-Over Risk

SIAM Activity Group on FME Virtual Talk Series Join us for a series of online talks on topics related to mathematical finance and engineering and running every two weeks until further notice. The series is organized by the SIAM Activity Group on Financial Mathematics and Engineering. Spea

From playlist SIAM Activity Group on FME Virtual Talk Series

Stanford CS229: Machine Learning | Summer 2019 | Lecture 13-Statistical Learning Uniform Convergence

For more information about Stanford’s Artificial Intelligence professional and graduate programs, visit: https://stanford.io/3py8nGr Anand Avati Computer Science, PhD To follow along with the course schedule and syllabus, visit: http://cs229.stanford.edu/syllabus-summer2019.html

From playlist Stanford CS229: Machine Learning Course | Summer 2019 (Anand Avati)

Climate risk analytics: Creating resilient infrastructure for stress testing and modelling

**Please note, due to unexpected technical issues, the audio around 03:30-05:30 crackles. We apologise for the inconvenience, and hope that the slides provided can help you with the content.** As we ramp up on initiatives from regulators and banks for climate risk regulations, net zero co

From playlist Webinars: At home with the experts

What's the main mistake that risk managers are making with conduct risk and compliance?

Peter Tyson, Head Of Conduct & Compliance, Standard Life, explains the key mistakes that risk managers are making with conduct and compliance at RiskMinds Insurance 2016.

From playlist Insurance risk: Predict risk in an unpredictable world

QRM L1-2: The dimensions of risk and friends

Welcome to Quantitative Risk Management (QRM). In this second video, we analyse the dimensions of risk. Risk is in fact an object that we need to consider from different points of view, and that sometimes we cannot even quantify. We will also discuss the importance of statistical thinking

From playlist Quantitative Risk Management