Financial Option Theory with Mathematica -- Volatility, and direct solution of PDEs

This is my third session of my track about Financial Option Theory with Mathematica. I first develop two methods to compute historical volatility of a stock. Next I do the same for an estimate of the historical appreciation rate. I then come to the very important topic of the implied volat

From playlist Financial Options Theory with Mathematica

The Volatility Smile - Options Trading Lessons

The volatility smile is a real-life pattern that is observed when different strikes of option, with the same underlying and same expiration date are plotted on a graph. These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. htt

From playlist The Term Structure of Volatility

2. Utilities, Endowments, and Equilibrium

Financial Theory (ECON 251) This lecture explains what an economic model is, and why it allows for counterfactual reasoning and often yields paradoxical conclusions. Typically, equilibrium is defined as the solution to a system of simultaneous equations. The most important economic mode

From playlist Financial Theory with John Geanakoplos

Gradient and directional derivative

Free ebook http://tinyurl.com/EngMathYT A lecture on the gradient and directional derivative of functions of two (or more) variables. Plenty of examples are discussed. The ideas find uses in applied mathematics, science and engineering.

From playlist Mathematics for Finance & Actuarial Studies 2

Matteo Burzoni: Viability and arbitrage under Knightian uncertainty

Abstract: We provide a general framework to study viability and arbitrage in models for financial markets. Viability is intended as the existence of a preference relation with the following properties: It is consistent with a set of preferences representing all the plausible agents trading

From playlist Probability and Statistics

Applied Portfolio Management - Class 3 - Equity Investment Management

All slides are available on my Patreon page: https://www.patreon.com/PatrickBoyleOnFinance In todays video we learn about equity investment management. We learn about how a portfolio manager builds a portfolio. We learn about the efficient market hypothesis, macroeconomic analysis, the

From playlist Applied Portfolio Management

What is Implied Volatility? Options Trading Tutorial.

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle

From playlist The Term Structure of Volatility

Principles of Evolution, Ecology and Behavior (EEB 122) Sex allocation is an organism's decision on how much of its reproductive investment should be distributed to male and female functions and/or offspring. Under most conditions, the optimal ratio is 50:50, but that can change under c

From playlist Evolution, Ecology and Behavior with Stephen C. Stearns

"Evolutionary Medicine" Sinauer Associates (2015) is the textbook that supports these lectures. Instructors can request examination copies and sign up to download figures here: http://www.sinauer.com/catalog/medical/evolutionary-medicine.html

From playlist Evolution and Medicine (2015) with Stephen Stearns

On the existence of thermodynamic potentials for quantum systems... by Takahiro Sagawa

PROGRAM CLASSICAL AND QUANTUM TRANSPORT PROCESSES : CURRENT STATE AND FUTURE DIRECTIONS (ONLINE) ORGANIZERS: Alberto Imparato (University of Aarhus, Denmark), Anupam Kundu (ICTS-TIFR, India), Carlos Mejia-Monasterio (Technical University of Madrid, Spain) and Lamberto Rondoni (Polytechn

From playlist Classical and Quantum Transport Processes : Current State and Future Directions (ONLINE)2022

In this video, I define a neat concept called the fractal derivative (which shouldn't be confused with fractional derivatives). Then I provide a couple of examples, and finally I present an application of this concept to the study of anomalous diffusion in physics. Enjoy!

From playlist Calculus

Unknown Market Wizards - Jack Schwager - The Worlds Greatest Unknown Traders

Market Wizards - Jack Schwager on the worlds greatest unknown traders. An interview with Jack Schwager, the author of The Market Wizards series of books, on his new book, Unknown Market Wizards. Jack has been involved in financial markets for over 45 years, he worked as a market analyst, a

From playlist Statistics For Traders

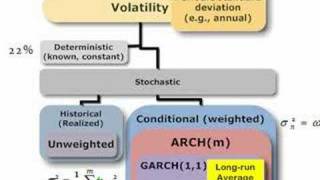

Lots of ways to estimate volatility. In this map, I parse out implied volatility (forward looking) and deterministic (constant) and focus on stochastic volatility: volatility that changes over time, either via (conditional) recent volatility and/or random shocks. For more financial risk vi

From playlist Volatility

Lecture 19 - Technical Analysis

This is Lecture 19 of the COMP510 (Computational Finance) course taught by Professor Steven Skiena [http://www.cs.sunysb.edu/~skiena/] at Hong Kong University of Science and Technology in 2008. The lecture slides are available at: http://www.algorithm.cs.sunysb.edu/computationalfinance/pd

From playlist COMP510 - Computational Finance - 2007 HKUST

Twenty third SIAM Activity Group on FME Virtual Talk Series

Date: Thursday, December 2, 2021, 1PM-2PM ET Speaker 1: Renyuan Xu, University of Southern California Speaker 2: Philippe Casgrain, ETH Zurich and Princeton University Moderator: Ronnie Sircar, Princeton Universit Join us for a series of online talks on topics related to mathematical fina

From playlist SIAM Activity Group on FME Virtual Talk Series

William McClain, “Origins of the Genetic Code and Transfer RNA Were Inextricably Linked”

Presentation by Dr. William McClain at the Sidney Altman Symposium held on March 24, 2016 at the Greenberg Center, Yale University.

From playlist The Sidney Altman Symposium

Building a Personalised Attrition Recommendation System

This webinar will cover an end-to-end study of attrition – the dwindling number of the workforce – in a company. The end goal of an attrition recommendation system is to develop retention strategies to prevent employee churn. In this session, we will discuss the process starting from data

From playlist Fundamentals of Machine Learning

Lecture: Numerical Differentiation Methods

From simple Taylor series expansions, the theory of numerical differentiation is developed.

From playlist Beginning Scientific Computing

Hypothesis Tests AS Level Maths Statistics Exam Questions 1

AS Level Maths Statistics Exam Questions on hypothesis tests with binomial distribution, from AQA, Edexcel and OCR MEI, perfect revision and practice for your AS Maths exams and A Level Maths year 1! Statistical hypothesis testing is a huge part of statistics in A Level Maths, and you'll

From playlist Hypothesis Tests AS Level Maths Statistics Exam Questions

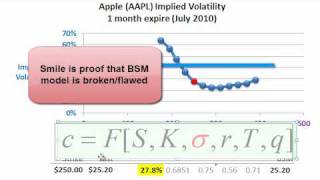

A plot of implied volatility (i.e., the volatility that forces the BSM model option price to equal the observed market price) against strike price. The smile is proof the model is imprecise (incorrect in some assumption); e.g., returns are not lognormally distributed. For more financial ri

From playlist Volatility