Statistics Lecture 7.2: Finding Confidence Intervals for the Population Proportion

https://www.patreon.com/ProfessorLeonard Statistics Lecture 7.2: Finding Confidence Intervals for the Population Proportion

From playlist Statistics (Full Length Videos)

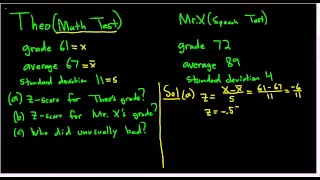

Computing z-scores(standard scores) and comparing them

Please Subscribe here, thank you!!! https://goo.gl/JQ8Nys Computing z-scores(standard scores) and comparing them

From playlist Statistics

How to find the 20th and 80th percentile of a data set

👉 Learn how to find the percentile of a data set. The kth percentile of a data set is the data value that appeared in the kth position after the dataset has been divided into 100 equal parts. Thus to find the kth percentile of a dataset, we first divide the dataset into 100 equal parts, an

From playlist Statistics

Determine the Percent of Data an Number of Values Below and Above a Quartile

This video explains how to determine the percent and number of values at or below as well as at or above a given quartile. http://mathispower4u.com

From playlist Statistics: Describing Data

Determine if the Given Value is from a Discrete or Continuous Data Set MyMathlab Statistics

Please Subscribe here, thank you!!! https://goo.gl/JQ8Nys Determine if the Given Value is from a Discrete or Continuous Data Set MyMathlab Statistics

From playlist Statistics

Statistics: Ch 4 Probability in Statistics (12 of 74) Relative VS Cumulative Relative Frequency

Visit http://ilectureonline.com for more math and science lectures! To donate: http://www.ilectureonline.com/donate https://www.patreon.com/user?u=3236071 We will graphically examine the differences between relative frequency vs cumulative relative frequency. Next video in this series c

From playlist STATISTICS CH 4 STATISTICS IN PROBABILITY

Statistics Lecture 3.4: Finding Z-Score, Percentiles and Quartiles, and Comparing Standard Deviation

https://www.patreon.com/ProfessorLeonard Statistics Lecture 3.4: Finding the Z-Score, Percentiles and Quartiles, and Comparing Standard Deviation

From playlist Statistics (Full Length Videos)

How to Create a Frequency Table – Simple, Cumulative, Relative Frequency & Percentile (3-3)

Now that we understand what frequency is, we will create a frequency table. The table will include columns for our variable, simple frequency, relative frequency, cumulative frequency, and percentiles. The term simple frequency refers to the number of times a score occurs in the data se

From playlist WK3 Frequency - Online Statistics for the Flipped Classroom

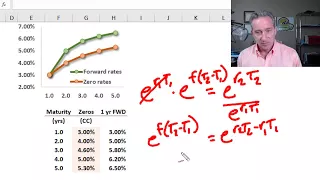

Forward rates are implied by zero rates (FRM T3-11)

[my xls is here https://trtl.bz/2HMQkUU] Forward rates link two zero (aka, spot) rates by ensuring your expected return is the same between two choices: (1) invest at the longer-term spot rate versus (2) invest at the shorter-term spot rate and "roll over" into the implied forward rate. Th

From playlist Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

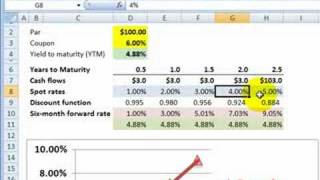

FRM: Comparison of spot curve, forward curve and bond yield

A simple comparison using a 2.5 year $100 par 6% semiannual coupon bond. Spot rate: the yield for each cash flow that treats the cash flow as a zero-coupon bond. A coupon-paying bond is a set of zero-coupon bonds. Forward rate: the implied forward rates that make an investor indifferent to

From playlist Bonds: Introduction

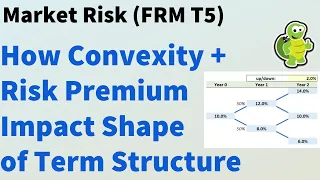

Convexity and risk premium impacts on shape of term structure (FRM T5-08)

In this video, I'm going to try to illustrate all of the important ideas that are in Tuckman's Chapter 8: The Evolution of Short Rates and the Shape of the Term Structure. This chapter discusses the shape of the term structure and the key influences on the shape of the spot rate term struc

From playlist Market Risk (FRM Topic 5)

Fixed Income: Infer discount factors, spot, forwards and par rates from swap rate curve (FRM T4-25)

Financial Risk Manager (FRM, Topic 4: Valuation and Risk Models, Fixed Income, Bruce Tuckman Chapter 2, Spot, Forward and Par Rates). Given the swap rate curve, we can infer the discount function (i.e., set of discount factors), spot rate curve, forward rate curve and par yield curve. Disc

From playlist Valuation and RIsk Models (FRM Topic 4)

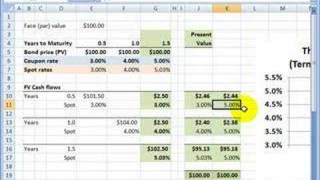

FRM: Calculate forward given spot rate

Given a 2.0 year spot and a 1.5 year spot, we want to solve for the six month forward staring in 1.5 years. That's the forward rate denoted by 1f3 or 0.5f1.5. For more financial risk management videos, visit our website! http://www.bionicturtle.com.

From playlist Bonds: Introduction

FRM: Bootstrapping the Treasury spot rate curve

The theoretical spot rate curve is different than the par yield curve. Here is how to bootstrap the spot rate. For more financial risk videos, visit our website! http://www.bionicturtle.com

From playlist Bonds: Introduction

Ses 5: Fixed-Income Securities II

MIT 15.401 Finance Theory I, Fall 2008 View the complete course: http://ocw.mit.edu/15-401F08 Instructor: Andrew Lo License: Creative Commons BY-NC-SA More information at http://ocw.mit.edu/terms More courses at http://ocw.mit.edu

From playlist MIT 15.401 Finance Theory I, Fall 2008

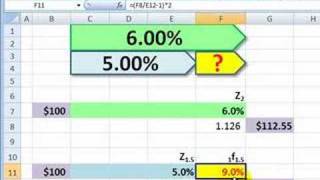

Implied forward rate under continuous compounding

Given two spot rates (e.g., 2 year and 1.5 year) we can infer the market implied forward rate (the six month rate in 1.5 years). Shown under discrete (semiannual) and continuous compounding.

From playlist Bonds: Introduction

Cumulative probability of default on risky bond

If we are given two spot rate term structures (spot rates for Treasuries and for risky corporate bond), the question is, what is the 2-year cumulative probability of default (PD)? We take THREE STEPS: 1. Compute 1-year forward rates; 2. Compute marginal probability of defaults; 3. Compute

From playlist Credit Risk: Introduction

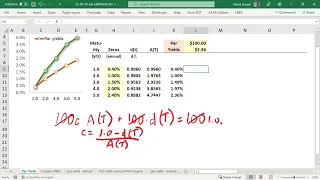

Why par yields are the best interest rate measure

Par yields are the best interest rate because they summarize the spot rate term structure into a single yield measure. I also show the so-called "coupon effect" which is also an argument in favor of par yields. But I think the better reason is their information content. Yield to maturity (

From playlist FRM applications

Irrigation Efficiencies - Part 1

From playlist TEMP 1