What is Skewness? | Statistics | Don't Memorise

What is Skewness in statistics? What are the different types of Skewness? ✅To learn more about Statistics, enroll in our full course now: https://infinitylearn.com/microcourses?utm_source=youtube&utm_medium=Soical&utm_campaign=DM&utm_content=XSSRrVMOqlQ&utm_term=%7Bkeyword%7D ✅Download

From playlist Middle School Math - Graphs and Statistics

What is skewness? A detailed explanation (with moments!)

See all my videos at http://www.zstatistics.com/videos/ 0:00 Introduction 4:28 Skewness calculation: Pearson 7:06 Skewness calculation: Moment-based 12:56 Skewness visualisation 14:02 Challenge question For the moment video, see here: http://www.zstatistics.com/descriptive-statistics/ (

From playlist Descriptive Statistics (13 videos)

How to find skewness in Excel with the SKEW function and Data Analysis. Works with all versions of Excel including 365, 2013, 2016.

From playlist Excel for Statistics

Statistics: Ch 6 The Normal Probability Distribution (2 of 28) The Skew Probability Curve

Visit http://ilectureonline.com for more math and science lectures! To donate: http://www.ilectureonline.com/donate https://www.patreon.com/user?u=3236071 We will learn what is a skew probability curve using the example of asking 100 households how many cars they have. Next video in thi

From playlist STATISTICS CH 6 THE NORMAL PROBABILITY DISTRIBUTION

Determining Skewness In Ogive Graphs

I help you identify left skewness, right skewness, and bell curves in an Ogive graph. At 6:40 I said "this is left skewed"- that is incorrect. Skewness is determined by the direction of the tail. In the histogram, the tail tapers off to the right, so it is right skewed. Check out http://w

From playlist AP Statistics

Skew-symmetric Matrix | Don't Memorise

This video explains the concept of a Skew-Symmetric Matrix. ✅To learn more about, Matrices, enroll in our full course now: https://infinitylearn.com/microcourses?utm_source=youtube&utm_medium=Soical&utm_campaign=DM&utm_content=uKPmyG18N7I&utm_term=%7Bkeyword%7D In this video, we will le

From playlist Matrices

Assumptions: Spotting SKEWNESS in a Distribution (6-2)

Skewness is a measure of the imbalance or asymmetry of a data distribution. The skewness value can be positive, zero, negative, or undefined. Skewness can be caused when outliers exist on one end of a distribution and pull the mean toward the outlier. The skew is in the tail of the distrib

From playlist Depicting Distributions from Boxplots to z-Scores (WK 6 QBA 237)

Skewness And Kurtosis And Moments | What Is Skewness And Kurtosis? | Statistics | Simplilearn

This video lecture on Skewness & Kurtosis will discuss symmetrical and skewed distribution. In addition, you will learn how to calculate Pearson's coefficient of skewness and what kurtosis is. Here we will discuss - 00:00 Symmetrical Distribution 01:12 Skewed Distribution 03:04 Pearson's

Skewed Distribution: left skewed vs right skewed

What does it mean for a distribution to be positively skewed, or negatively skewed?

From playlist Probability Distributions

The skew (and sample skew) of a distribution (FRM T2-6)

The skew is the third central moment divided by the cube of the standard deviation. Here I calculate skew using the binomial distribution. Discuss this video here in our FRM forum! https://trtl.bz/2Jrg0HP Subscribe here https://www.youtube.com/c/bionicturtle?sub-confirmation=1 to be notif

From playlist Quantitative Analysis (FRM Topic 2)

Level 1 Chartered Financial Analyst (CFA ®): Measures of dispersion including volatility

Session 2, Reading 8 (Part 2): A previous video in this CFA playlist looked at classic measures of central tendency. This is also called the first moment of the distribution or the distributions the location where is the distribution centered. When we say that I think most of us think of t

From playlist Level 1 Chartered Financial Analyst (CFA ®) Volume 1

Prospect Theory and Stock Market Anomalies - L. Jin - 1/31/2020

"Prospect Theory and Stock Market Anomalies" Lawrence Jin, Assistant Professor of Finance, Caltech Abstract: This talk discusses some recent development in the field of behavioral finance, with a focus on a new model of asset prices in which investors evaluate risk according to prospect t

From playlist HSS Caltech + Finance 2020

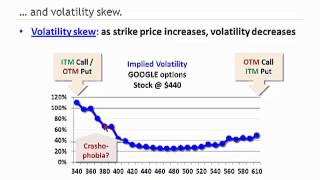

The Volatility Smile - Options Trading Lessons

The volatility smile is a real-life pattern that is observed when different strikes of option, with the same underlying and same expiration date are plotted on a graph. These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. htt

From playlist The Term Structure of Volatility

Kurtosis of a probability distribution (FRM T2-7)

[Here is my xls http://trtl.bz/121817-yt-kurtosis-xls] Kurtosis is the standardized fourth central moment and is a measure of tail density; e.g., heavy or fat-tails. Heavy-tailedness also tends to correspond to high peakedness. Excess kurtosis (aka, leptokurtosis) is given by (kurtosis-3).

From playlist Quantitative Analysis (FRM Topic 2)

2012 FRM Market Risk Measurement & Management T5.a

This is a sample of our 2012 FRM Market Risk Measurement & Management T5.a video tutorials. You may view our products here: https://www.bionicturtle.com/products/financial-risk-management/ The Bionic Turtle program is the most effective and affordable preparation aid for the Financial Ri

From playlist FRM

QRM 5-2: The problem of estimating the tail

Welcome to Quantitative Risk Management (QRM). Let us finish our discussion about the graphical tools we can use to study tails. We briefly discuss the Moment Ratio Plot and the Zenga Plot. After that we address the problem of estimating the tail parameter, using MLE and other approaches.

From playlist Quantitative Risk Management

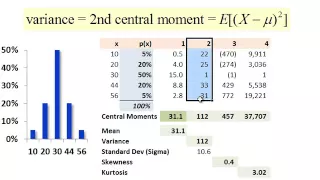

FRM: Distribution moments (mean, variance, skew, kurtosis)

Here is the spreadsheet I used @ http://db.tt/bziK312h. The four central moments of a distribution are mean (1st), variance, skew and kurtosis. They tell us quickly about the personality of the distribution. For more financial risk videos, visit our website! http://www.bionicturtle.com.

From playlist Operational Risk Analytics

Binomial test: if Elon Musk samples 100 twitter accounts, how many bots (fakes) are too many?

Elon Musk is holding up his twitter purchase to investigate their claim that only 5.0% of the accounts on the platform are fake. If he samples 100 accounts, how many is too many; i.e., at what number should he reject the null hypothesis? Subscribe here https://www.youtube.com/c/bionicturt

From playlist FRM applications

Skew Lines, Perpendicular & Parallel Lines & Planes, Intersecting Lines & Transversals

This geometry video tutorial provides a basic introduction into skew lines. It explains the difference between parallel lines, perpendicular lines, skew lines, intersecting lines, and transversals. Parallel lines are coplanar lines that do not intersect. Skew lines are noncoplanar lines

From playlist Geometry Video Playlist

STAT 200 Lesson 2 Lecture Video

Table of Contents: 00:48 - Review 03:16 - 1. Compute and interpret a basic proportion/risk/probability and odds 08:05 - 2. Select and interpret visual representations for one categorical variable, two categorical variables, and one quantitative variable 15:25 - 3. Use Minitab Express to

From playlist STAT 200 Video Lectures