FinMath L3-2: Risk-neutral measures and self-financing portfolios

Welcome to Lesson 3 of Financial Mathematics (Part 2). In this second half of the lesson, we discuss important topics like self-financing portfolio, risk neutral measures and their basic properties, and the concept of arbitrage. All these tools are essential in financial mathematics, and t

From playlist Financial Mathematics

How Self Storage Thrives Off The American Dream

Start your business today with a free trial of Shopify - go to https://www.shopify.com/modernmba to learn more. Self-service storage is an American phenomenon. While self-storage facilities exist in Europe and Asia, the business overseas does not come close to the scale and demand in the

From playlist Season 2

This video explains the math behind investing in mutual funds. It discusses the value of a mutual fund's annual performance and the value of investing long term. A equity mutual fund is a financial vehicle that invests in a variety of stocks. Thus a mutual fund is a passive way for an i

From playlist Stocks and Bonds

Evergrande Wealth Management Products - A Ponzi Scheme?

In an interview with local media, an Evergrande financial adviser said the products were a type of “supply chain finance”. While the money from retail investors may in years past have gone to its suppliers, the Evergrande executives in Shenzhen receiving retail investors said this was no l

From playlist What is Happening In The Market?

From playlist Personal Finance

Applied Portfolio Management - Video 4 - Fixed Income Asset Management

All slides are available on my Patreon page: https://www.patreon.com/PatrickBoyleOnFinance Fixed income refers to any type of investment under which the borrower or issuer is obliged to make payments of a fixed amount on a fixed schedule. For example, the borrower may have to pay interest

From playlist Applied Portfolio Management

Low Default Portfolios (Part 1)

A Low Default Portfolio (LDP) is a portfolio characterized by a low number of defaults. Too simple? Citing the BCBS (Basel Committee on Banking Supervision): Several types of portfolios may have low numbers of defaults. For example, some portfolios historically have experienced low numb

From playlist Topics in Credit Risk Modelling

Fin Math L5-3: Towards Black-Scholes-Merton

Welcome to the last part of Lesson 5. In this video we cover some last relevant topics to finally deal with the Black-Scholes-Merton theorem, which will be the starting point of all our pricing exercises. Here you can download the new chapter of the lecture notes: https://www.dropbox.com/s

From playlist Financial Mathematics

To have sound levels of self-esteem is one of the gateways to happiness. But achieving this has very little to do with the progress of our careers. If you like our films, take a look at our shop (we ship worldwide): https://goo.gl/1Uj9JM Watch more films on SELF: http://bit.ly/TSOLself P

From playlist SELF

Financial Derivatives - Lecture 8 - Monte Carlo Method & Risk Management

These full length lectures are being provided for students who are unable to attend live university lectures due to the public health issues associated with Covid 19. I will return to my standard YouTube video format shortly. Buy The Book Here: https://amzn.to/2Qdj9zu Visit our website.

From playlist Full Financial Derivatives Lectures

Fin Math L6-1: The Black-Scholes-Merton theorem

Welcome to Lesson 6 of Financial Mathematics. This is the lesson of the Black-Scholes-Merton (BSM) theorem. Finally, you might say. But it will also be the lesson of volatility and distortions. A lot of interesting things. In this first video, we focus on the BSM theorem. Topics: 00:00 I

From playlist Financial Mathematics

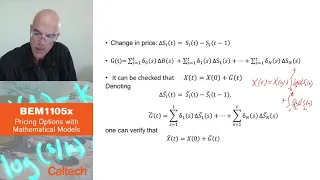

BEM1105x Course Playlist - https://www.youtube.com/playlist?list=PL8_xPU5epJdfCxbRzxuchTfgOH1I2Ibht Produced in association with Caltech Academic Media Technologies. ©2020 California Institute of Technology

From playlist BEM1105x Course - Prof. Jakša Cvitanić

Personal Finance Quiz 0 Question 05

These videos cover questions from one of assessments. It covers basics in federal, state, medicare and social security taxes and how them impact monthly income. IT also covers the idea of micro-finance. To see our other personal finance videos, go here: https://www.youtube.com/playlist?li

From playlist Personal Finance

[See Description] Programming for Finance Part 2 - Creating an automated trading strategy

UPDATED series: https://pythonprogramming.net/quantopian-trading-strategies-introduction-python-programming-for-finance/ This series has become outdated with Quantopian 2.0. In this tutorial, we break down the major elements to creating and testing an automated trading strategy, using Q

From playlist Python for Finance with Zipline and Quantopian

1. Finance and Insurance as Powerful Forces in Our Economy and Society

Financial Markets (ECON 252) Professor Shiller provides a description of the course, Financial Markets, including administrative details and the topics to be discussed in each lecture. He briefly discusses the importance of studying finance and each key topic. Lecture topics will includ

From playlist Financial Markets (2008) with Robert Shiller

Paolo Guasoni, Lesson III - 20 december 2017

QUANTITATIVE FINANCE SEMINARS @ SNS PROF. PAOLO GUASONI TOPICS IN PORTFOLIO CHOICE

From playlist Quantitative Finance Seminar @ SNS

Daniel Balint: Discounting invariant FTAP for large financial markets

Abstract: For large financial markets as introduced in Kramkov and Kabanov 94, there are several existing absence-of-arbitrage conditions in the literature. They all have in common that they depend in a crucial way on the discounting factor. We introduce a new concept, generalizing NAA1 (K

From playlist Probability and Statistics

🔥Career Masterclass: Learn about the Caltech CTME Cloud Computing Bootcamp | Simplilearn

🔥Explore more about the Course here: https://www.simplilearn.com/pgp-cloud-computing-certification-training-course?utm_campaign=CloudComputingWebinar15Feb2023&utm_medium=Description&utm_source=youtube Career Masterclass: Learn about the Caltech CTME Cloud Computing Bootcamp a live and int

From playlist Simplilearn Live