This came as a surprise. Although it looks like an example with smooth time-stepping, it is not. It is with original, simple time-stepping. I'm not exactly sure what this means. Maybe my smooth time-stepping method is superfluous.

From playlist SmoothLife

Felix Otto: Singular SPDE with rough coefficients

Abstract: We are interested in parabolic differential equations (∂t−a∂2x)u=f with a very irregular forcing f and only mildly regular coefficients a. This is motivated by stochastic differential equations, where f is random, and quasilinear equations, where a is a (nonlinear) function of u.

From playlist Probability and Statistics

Peter Friz: Some examples of homogenization related rough paths

Find this video and other talks given by worldwide mathematicians on CIRM's Audiovisual Mathematics Library: http://library.cirm-math.fr. And discover all its functionalities: - Chapter markers and keywords to watch the parts of your choice in the video - Videos enriched with abstracts, b

From playlist SPECIAL 7th European congress of Mathematics Berlin 2016.

David Kelly: Fast slow systems with chaotic noise

Find this video and other talks given by worldwide mathematicians on CIRM's Audiovisual Mathematics Library: http://library.cirm-math.fr. And discover all its functionalities: - Chapter markers and keywords to watch the parts of your choice in the video - Videos enriched with abstracts, b

From playlist Probability and Statistics

Multiple-Scattering Microfacet BSDFs with the Smith Model

The paper "Multiple-Scattering Microfacet BSDFs with the Smith Model" is available here: https://eheitzresearch.wordpress.com/240-2/ Update: it is being added to Blender's Cycles! - https://developer.blender.org/D2002 Modeling multiple scattering in microfacet theory is considered an imp

From playlist Light Transport, Ray Tracing and Global Illumination (Two Minute Papers)

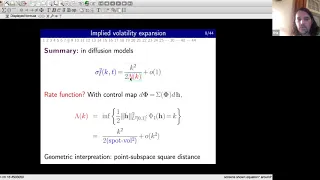

Peter Friz (TU and WIAS Berlin) -- Laplace method on rough path and model space

Laplace's method allows one to obtain precise asymptotics in the large deviation principle. I will review the case of rough paths, then talk about extensions to rough volatility and singular SPDEs. Joint work with Paul Gassiat (Paris), Paolo Pigato (Rom) and Tom Klose (Berlin).

From playlist Columbia SPDE Seminar

Josef Teichmann: An elementary proof of the reconstruction theorem

CIRM VIRTUAL EVENT Recorded during the meeting "Pathwise Stochastic Analysis and Applications" the March 09, 2021 by the Centre International de Rencontres Mathématiques (Marseille, France) Filmmaker: Guillaume Hennenfent Find this video and other talks given by worldwide mathematician

From playlist Virtual Conference

Android Development for Beginners 11

Get the vector art here : http://goo.gl/y8HTCp Best Android Book : http://goo.gl/uPhXFI In this part of my App Inventor tutorial I will start covering Android interface design. I want the weather app we have been creating in parts 9 and 10 of this series to look very nice. Here I'll sho

From playlist Android Development for Beginners

NASA’s Perseverance Mars Rover Team to Discuss Early Science, Sample Collection (News Briefing)

Members from NASA’s Perseverance Mars rover team will discuss early science results from the robotic scientist and its preparations to collect the first-ever Martian samples for planned return to Earth. A key objective for Perseverance’s mission to Mars is astrobiology, including the searc

From playlist Mars

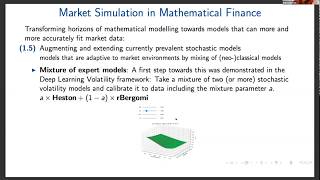

Second SIAM Activity Group on FME Virtual Talk

This is the second in a series of online talks on topics related to mathematical finance and engineering. The series is organized by the SIAM Activity Group on Financial Mathematics and Engineering. Title: A Data-driven Market Simulator for Small Data Environments Abstract: In this talk w

From playlist SIAM Activity Group on FME Virtual Talk Series

Mathworks Excellence in Innovation Project 209 : Autonomous Navigation of Vehicle in Rough terrain

This is a demonstration of the implementation of Autonomous Navigation of a robot using Gazebo simulation and Matlab Simulink models The detailed documentation of this project is available below: https://github.com/mathworks/MathWorks-Excellence-in-Innovation/tree/main/projects/Autonomou

From playlist MathWorks Excellence in Innovation