QRM L1-1: The Definition of Risk

Welcome to Quantitative Risk Management (QRM). In this first class, we define what risk if for us. We will discuss the basic characteristics of risk, underlining some important facts, like its subjectivity, and the impossibility of separating payoffs and probabilities. Understanding the d

From playlist Quantitative Risk Management

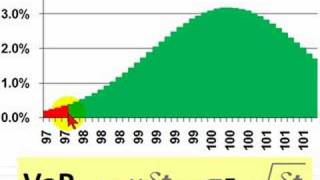

What is Value at Risk? VaR and Risk Management

In todays video we learn about Value at Risk (VaR) and how is it calculated? Buy The Book Here: https://amzn.to/37HIdEB Follow Patrick on Twitter Here: https://twitter.com/PatrickEBoyle What Is Value at Risk (VaR)? Value at risk (VaR) is a calculation that aims to quantify the level of

From playlist Risk Management

FRM: Parametric value at risk (VaR): Pros & Cons

Here is a quick explanation of parametric value at risk (VaR) as a means to illustrating its strengths/weaknesses. Please note: The essence of parametric VaR is "no data:" while historical data is surely used to select a distribution and calibrate its parameters, a parametric VaR leans on

From playlist Value at Risk (VaR): Introduction

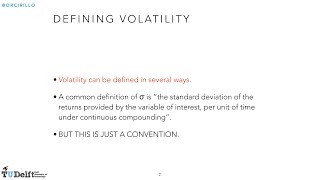

Risk Management Lesson 4A: Volatility

First part of Lesson 4. Topics: - Definitions of volatility - Basic assumptions (do they hold?) - Arch and G-arch models (brief overview)

From playlist Risk Management

Risk Management Lesson 5A: Value at Risk

In this first part of Lesson 5, we discuss Value-at-Risk (VaR). Topics: - Definition of VaR - Loss distribution and confidence level - The normal VaR

From playlist Risk Management

Alan Smith: What are the greatest risks in the post-Brexit world?

Alan Smith, Global Head of Risk Strategy at HSBC, speaking at Risk Minds International 2016 on the greatest risks in the Post-Brexit world. Find out more at https://goo.gl/KVtbtC.

From playlist RiskMinds 2016

How do you calculate value at risk? Two ways of calculating VaR

In todays video we learn how to calculate VaR or Value at Risk. Buy The Book Here: https://amzn.to/37HIdEB Follow Patrick on Twitter Here: https://twitter.com/PatrickEBoyle What is VAR? The most popular and traditional measure of risk is volatility. The main problem with volatility, how

From playlist Risk Management

Chris Matten at Risk Minds International 2015 | The risk management industry's biggest challenge

Chris Matten, Partner, Singapore Risk Assurance Practice at PwC, speaking at Risk Minds International 2015 in Amsterdam on the biggest challenge facing the risk management industry.

From playlist RiskMinds Live 2015

QRM L1-2: The dimensions of risk and friends

Welcome to Quantitative Risk Management (QRM). In this second video, we analyse the dimensions of risk. Risk is in fact an object that we need to consider from different points of view, and that sometimes we cannot even quantify. We will also discuss the importance of statistical thinking

From playlist Quantitative Risk Management

Fin Math L8-2: Conditions for the absence of arbitrage

Welcome to Financial Mathematics. In the second video of lesson 8 we consider some necessary conditions for the absence of arbitrage on the market. For example we discuss the Put-Call Parity, and the impossibility of having two (or more) risk-free assets. Topics: 00:00 Welcome 03:55 Uniq

From playlist Financial Mathematics

Interest rate parity applies cost of carry model (FRM T3-21)

[my xls is here https://trtl.bz/2uIVV9R] Interest rate parity applies the cost of carry (COC) model to enforce an equilibrium (indifference) between two choices: 1. translate the 1,000 EURs immediately at the spot FX rate, and subsequently grow them at the USD risk-free rate for two years;

From playlist Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013 View the complete course: http://ocw.mit.edu/18-S096F13 Instructor: Jake Xia This lecture focuses on portfolio management, including portfolio construction, portfolio theory, risk parity portfolios, and their limita

From playlist MIT 18.S096 Topics in Mathematics w Applications in Finance

What is Put Call Parity? How does it work?

Today we will learn about put call parity and how it works, These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https

From playlist Class 2: An Introduction to Options

Exotic options: chooser option (FRM T3-43)

The chooser (aka, as you like it) option has one strike price (K = $40.00 in my example) but two key dates (T1 and T2). On the first date (T1), the holder "chooses" it to be either a call or a put. At that point, it becomes a standard call/put with a remaining life of Δt = T2 - T1. In the

From playlist FM&P: Intro to Derivatives: Exotic options (FRM Topic 3)

Just machine learning In this talk, I will address some concerns about the use of machine learning in situations where the stakes are high (such as criminal justice, law enforcement, employment decisions, credit scoring, health care, public eligibility assessment, and school assignments).

From playlist DSI Virtual Seminar Series

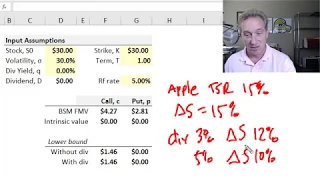

Lower bounds for European stock option prices (FRM T3-35)

[here is the xls https://trtl.bz/2BYKn6P] The lower bound for the price of a European call option is given by max[0, S(0) - K*exp(-rT) - D]. The lower bound for the price of a European put option is given by max[0, K*exp(-rT) - S(0) + D], where D is the lump-sum PV of the dividend. Where q

From playlist Financial Markets and Products: Option Trading Strategies (FRM Topic 3, Hull Ch 10-12)

[my XLS is here https://trtl.bz/2IzY0ui] We can synthesize stock ownership with a synthetic forward plus cash: S(0) = (c-p) + K*exp(-rT). That's put-call parity! My memorization mnemonic is "call plus cash equals protective put:" c + K*exp(-rt) = p + S(0). Discuss this video here in our FR

From playlist Financial Markets and Products: Option Trading Strategies (FRM Topic 3, Hull Ch 10-12)

Risk Management Lesson 4B: Volatility (second part) and Coherent Risk Measures

This is the second half of Lesson 4. Topics: - Exercise about volatility modeling with G-arch - Coherent risk measures - Are the variance and the standard deviation coherent? A useful document for you is available here: https://www.dropbox.com/s/6pdygf0bw6bcce1/coherence.pdf

From playlist Risk Management

Put-call parity arbitrage I | Finance & Capital Markets | Khan Academy

Courses on Khan Academy are always 100% free. Start practicing—and saving your progress—now: https://www.khanacademy.org/economics-finance-domain/core-finance/derivative-securities/put-call-options/v/put-call-parity-arbitrage-i Put-Call Parity Arbitrage I. Created by Sal Khan. Watch the

From playlist Options, swaps, futures, MBSs, CDOs, and other derivatives | Finance and Capital Markets | Khan Academy