QRM L1-1: The Definition of Risk

Welcome to Quantitative Risk Management (QRM). In this first class, we define what risk if for us. We will discuss the basic characteristics of risk, underlining some important facts, like its subjectivity, and the impossibility of separating payoffs and probabilities. Understanding the d

From playlist Quantitative Risk Management

FRM: Parametric value at risk (VaR): Pros & Cons

Here is a quick explanation of parametric value at risk (VaR) as a means to illustrating its strengths/weaknesses. Please note: The essence of parametric VaR is "no data:" while historical data is surely used to select a distribution and calibrate its parameters, a parametric VaR leans on

From playlist Value at Risk (VaR): Introduction

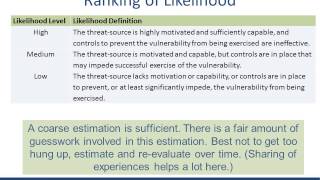

Risk Assessment: Likelihood Determination

http://trustedci.org/ Determining Likelihood of a threat as part of a cyber risk assessment.

From playlist Center for Applied Cybersecurity Research (CACR)

A look at RiskMinds Insurance 2017 so far...

Follow the conversation on Twitter @RiskMinds with #RMInsurance. Visit knect365.com/riskminds for the latest in Risk thought leadership.

From playlist RiskMinds Insurance 2017

QRM L1-2: The dimensions of risk and friends

Welcome to Quantitative Risk Management (QRM). In this second video, we analyse the dimensions of risk. Risk is in fact an object that we need to consider from different points of view, and that sometimes we cannot even quantify. We will also discuss the importance of statistical thinking

From playlist Quantitative Risk Management

What is Value at Risk? VaR and Risk Management

In todays video we learn about Value at Risk (VaR) and how is it calculated? Buy The Book Here: https://amzn.to/37HIdEB Follow Patrick on Twitter Here: https://twitter.com/PatrickEBoyle What Is Value at Risk (VaR)? Value at risk (VaR) is a calculation that aims to quantify the level of

From playlist Risk Management

Welcome to Quantitative Risk Management (QRM). In this lesson we introduce the axiomatic approach to risk measures. We give the definition of risk measure and we discuss what its uses for us are in terms of reserve capital quantification. We then define coherent and convex measures. The p

From playlist Quantitative Risk Management

Cathy O'Neil interviewed at Strata Jumpstart 2011

Cathy O'Neil earned a Ph.D. in math from Harvard, was postdoc at MIT in the math department, and a professor at Barnard College where she published a number of research papers in arithmetic algebraic geometry. She then chucked it and switched over to the private sector. She worked as a qua

From playlist Strata NY 2011

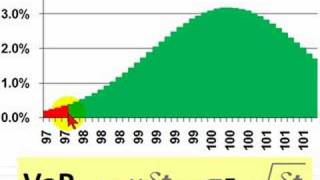

FRM: Hybrid historical simulation approach to value at risk (VaR)

Yesterday I illustrated the simple historical approach to estimating value at risk (VaR). Today, using the same 100-day sample of Google's recent daily (periodic) stock returns, I illustrate the hybrid approach. The key idea is: Under the simple, each daily return gets the same weight (1%)

From playlist Value at Risk (VaR): Introduction

Peter Arndt - Ranges of functors and geometric classes via topos theory

Talk at the school and conference “Toposes online” (24-30 June 2021): https://aroundtoposes.com/toposesonline/ Slides: https://aroundtoposes.com/wp-content/uploads/2021/07/ArndtSlidesToposesOnline.pdf We explore criteria for the axiomatizability of images of functors by kappa-geometric s

From playlist Toposes online

Overview of various methods for sensitivity analysis in the UQ of subsurface systems

From playlist Uncertainty Quantification

Introducing: RiskMinds in Focus

What does it take to be a leading risk mind in 2021? Managing uncertainty, technology risk and regulatory developments. A virtual week of precision-engineered content laser-focused on how risk managers can add value and enable business transformation. Join the days that matter to you. Me

From playlist RiskMinds 2021

How To Protect Your Online Privacy With A Threat Model | Tutorial 2022

Privacy tutorial with a threat model methodology. This will help you achieve strong privacy consistently and reliably. Support independent research: https://www.patreon.com/thehatedone Privacy tools are inconsistent. The inventory of recommended countermeasures changes all the time. On t

From playlist Security by compartmentalization - learn to protect your privacy effectively

Memory effects in Kardar Parisi Zhang growth: exact results via the by Pierre Le Doussal

Date: Thursday, October 12, 2017 Time: 11:00 AM Venue: Madhava Lecture Hall, ICTS Campus, Bangalore Abstract : We review recent progress in describing the statistics of height fluctuations in 1D Kardar Parisi Zhang (KPZ) growth, focusing on the KPZ equation and its integrability propert

From playlist ICTS Colloquia