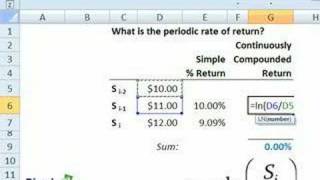

Intro to Quant Finance: Periodic Rate of Return

Periodic rate of return

From playlist Intro to Quant Finance

Ex: Find the Sale Tax Percentage

This video explains how to determine the sales tax percent given the amount paid and the sale price. Search Complete Library at http://www.mathispower4u.wordpress.com

From playlist Percent Applications

Determine the Total Return of an Investment as Percent

This video explains how to calculate the total return on an investment as a percent. http://mathispower4u.com

From playlist Finance: Simple and Compounded Interest

Unit 5 - practice problem 3 question

From playlist Courses and Series

Annual Rate of Return Need for Loss Recover and Additional Return on Investment

This video explains what rate of return is needed to recover from a loss as well as the rate of return needed to earn a certain rate of return moving forward. https://mathispower4u.com

From playlist Finance: Simple and Compounded Interest

How To Calculate Your Average Cost Basis When Investing In Stocks

This video tutorial explains how to calculate the average cost basis or average cost per share when making multiple investment purchases of the same stock at different prices. Stock Trading Strategies For Beginners: https://www.youtube.com/watch?v=7IBzTZqeyo0 Call and Put Options: https:

From playlist Stocks and Bonds

Ex: Find the Percent of an Amount - Sale Tax

This video explains how to solve a percent problem by determining the percent of a number. http://mathispower4u.com

From playlist Percent Applications

FRM: Time-weighted versus dollar-weighted (IRR) returns

Time-weighted returns (TWR) vs Dollar-weighted returns (DWR). For more Financial Risk Management videos, visit our website at http://www.bionicturtle.com!

From playlist FRM

Ses 12: Options III & Risk and Return I

MIT 15.401 Finance Theory I, Fall 2008 View the complete course: http://ocw.mit.edu/15-401F08 Instructor: Andrew Lo License: Creative Commons BY-NC-SA More information at http://ocw.mit.edu/terms More courses at http://ocw.mit.edu

From playlist MIT 15.401 Finance Theory I, Fall 2008

Here I explain an idea that is confusing the first time you see it: a variable is lognormally distributed if its log (or natural log) is normally distributed. I use an example of future stock price: it the rate of return is normally distributed (it can be negative), the future stock price

From playlist Statistics: Distributions

MIT 15.401 Finance Theory I, Fall 2008 View the complete course: http://ocw.mit.edu/15-401F08 Instructor: Andrew Lo License: Creative Commons BY-NC-SA More information at http://ocw.mit.edu/terms More courses at http://ocw.mit.edu

From playlist MIT 15.401 Finance Theory I, Fall 2008

Lecture 13 - Financial Time Series Data

This is Lecture 13 of the COMP510 (Computational Finance) course taught by Professor Steven Skiena [http://www.cs.sunysb.edu/~skiena/] at Hong Kong University of Science and Technology in 2008. The lecture slides are available at: http://www.algorithm.cs.sunysb.edu/computationalfinance/pd

From playlist COMP510 - Computational Finance - 2007 HKUST

Yield to Maturity Interpretations (FRM T3-10)

[my xls is here https://trtl.bz/2HifflO] Superficially, the yield to maturity (YTM, aka yield) simply inverts the usual time value of money (TVM) inputs by solving for the yield as a function of four inputs: face (future) value, coupon (payment), maturity (time), and current price (present

From playlist Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

Ses 13: Risk and Return II & Portfolio Theory I

MIT 15.401 Finance Theory I, Fall 2008 View the complete course: http://ocw.mit.edu/15-401F08 Instructor: Andrew Lo License: Creative Commons BY-NC-SA More information at http://ocw.mit.edu/terms More courses at http://ocw.mit.edu

From playlist MIT 15.401 Finance Theory I, Fall 2008

Contango versus normal backwardation (FRM T3-20)

In the case of a consumption commodity (e.g., corn, copper) we expected to observe contango: F(0) exceeds S(0). Contango implies (i) the cost of carry exceeds the convenience yield, and identically (ii) the risk-free rate exceeds the lease rate. We also might expect normal backwardation: F

From playlist Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

How to Use the Capital Asset Pricing Model (CAPM) to Value Investments

If you like this video, drop a comment, give it a thumbs up and consider subscribing here: https://www.youtube.com/c/HowToBeAnAdult?sub_confirmation=1 Read more on the Capital Asset Pricing Model and DOWNLOAD the FREE Excel file here: https://magnimetrics.com/capital-asset-pricing-model-c

From playlist Excel Tutorials

Dollar Cost Averaging - A Passive Stock Investment Strategy

This video tutorial provides a basic introduction into dollar cost averaging - a passive stock investment strategy that allows you to earn a decent return when a stock or a mutual fund is in an uptrend. This strategy neutralizes the effect of short term volatility and takes the guesswork

From playlist Stocks and Bonds

Applied Portfolio Management - Class 2 - Asset Classes & Returns

All slides are available on my Patreon page: https://www.patreon.com/PatrickBoyleOnFinance Todays class is all about investment asset classes. We examine the different types of investment an investor can put their savings in and try to work out the expected return of these asset classes,

From playlist Applied Portfolio Management