Determining The Value of an Annuity

This video defines an annuity and uses a formula to determine the value of an annuity over a period of time. http://mathispower4u.wordpress.com/

From playlist Financial Math

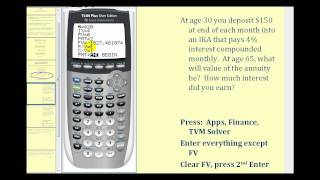

Determining The Value of an Annuity on the TI84

This video defines an annuity and uses the TI84 to determine the value of an annuity over a period of time. http://mathispower4u.wordpress.com/

From playlist Finance: Simple and Compounded Interest

Excel Busn Math 59: Annuities Math & Excel

Download Excel File: https://people.highline.edu/mgirvin/YouTubeExcelIsFun/135ch10.xls Download pdf file: https://people.highline.edu/mgirvin/YouTubeExcelIsFun/Busn135Ch10001.pdf Learn what an annuity is and how to make calculations for annuities. Future Value and Present Value Annuities

From playlist Excel Business Math 10: Annuities Math & Excel

Derive the Value of an Annuity Formula (Compounded Interest)

This video explains how to derive the value of an annuity formula using the case when deposits are made annually with interest compounded annually. Site: http://mathispower4u.com Blog: http://mathispower4u.wordpress.com

From playlist Finance: Simple and Compounded Interest

How To Calculate The Future Value of an Ordinary Annuity

This finance video tutorial explains how to calculate the future value of an ordinary annuity using a formula. You need to know the amount of money being deposited, the interest rate, and the number of years. My Website: https://www.video-tutor.net Patreon Donations: https://www.patreo

From playlist Personal Finance

Business Math - Finance Math (10 of 30) Future Value of an Annuity (End of Pay Period)

Visit http://ilectureonline.com for more math and science lectures! In this video I will explain and give an example of future value of an annuity (end of pay period). Next video in this series can be seen at: http://youtu.be/rz8iSkhM900

From playlist BUSINESS MATH 2 FINANCE MATH

Business Math - Finance Math (15 of 30) The Present Value of an Annuity

Visit http://ilectureonline.com for more math and science lectures! In this video I will explain and find the present value of an annuity. Next video in this series can be seen at: http://youtu.be/AuAf4nySLH8

From playlist BUSINESS MATH 2 FINANCE MATH

Tor vs VPN | Which one should you use for privacy, anonymity and security

Ultimate comparison between Tor and Virtual Private Networks - which one is better for anonymity, privacy and security? Which should you trust and use? Support me through Patreon: https://www.patreon.com/thehatedone - or donate anonymously: Monero: 84DYxU8rPzQ88SxQqBF6VBNfPU9c5sjDXfTC1

From playlist Analyses

Risk and Credit 500 Years Before Modern Finance - Francesca Trivellato

Followed by a discussion with IAS Academic Trustee Lorraine Daston.

From playlist Historical Studies

Estate Planning in Uncertain Times

October 21, 2011 - In December of 2010 Congress passes legislation that determined the estate and gift tax for 2010 through 2012. The director of Principal Gifts at Stanford, Howard Pearson looks at how you should handle estate planning and what techniques fit best under the current circum

From playlist Reunion Homecoming

24. Market Failures II: Informational Asymmetry

MIT 14.01 Principles of Microeconomics, Fall 2018 Instructor: Prof. Jonathan Gruber View the complete course: https://ocw.mit.edu/14-01F18 YouTube Playlist: https://www.youtube.com/playlist?list=PLUl4u3cNGP62oJSoqb4Rf-vZMGUBe59G- This lecture covers the topic of social insurance, which is

From playlist MIT 14.01 Principles of Microeconomics, Fall 2018

Financial Theory (ECON 251) This lecture continues the analysis of Social Security started at the end of the last class. We describe the creation of the system in 1938 by Franklin Roosevelt and Frances Perkins and its current financial troubles. For many democrats Social Security is th

From playlist Financial Theory with John Geanakoplos

Ses 3: Present Value Relations II

MIT 15.401 Finance Theory I, Fall 2008 View the complete course: http://ocw.mit.edu/15-401F08 Instructor: Andrew Lo License: Creative Commons BY-NC-SA More information at http://ocw.mit.edu/terms More courses at http://ocw.mit.edu

From playlist MIT 15.401 Finance Theory I, Fall 2008

MATH1050 Lec 33 Annuities and Installment Buying College Algebra with Dennis Allison

See full course at: https://cosmolearning.org/courses/college-algebra-pre-calculus-with-dennis-allison/ Video taken from: http://desource.uvu.edu/videos/math1050.php Lecture by Dennis Allison from Utah Valley University.

From playlist UVU: College Algebra with Dennis Allison | CosmoLearning Math

Gregory Miller interviewed at OSCON 2010

http://www.oscon.com Greg is a Co-Executive Director of the OSDV Foundation. He brings 24+ years experience in the tech sector, divided between software development and technology business development. He is also a (non practicing) IP lawyer involved in Internet & technology public poli

From playlist OSCON 2010

MIT 15.S08 FinTech: Shaping the Financial World, Spring 2020 Instructor: Prof. Gary Gensler View the complete course: https://ocw.mit.edu/15-S08S20 YouTube Playlist: https://www.youtube.com/playlist?list=PLUl4u3cNGP61Q_RVDn6srWbLV_zFnd9n0 This class covers the opportunities and challenges

From playlist MIT 15.S08 FinTech: Shaping the Financial World, Spring 2020

SOURCE Barcelona 2010: Anonymity, Privacy, and Circumvention with Tor in the Real World

Speaker: Sebastian Hahn The Tor network is the largest and well known anonymity network ever deployed.How does it work? Who uses it, where do they use it, and why do they use it? This talk will give a quick introduction to the Tor network, it will include real life examples of people usin

From playlist SOURCE Barcelona 2010

Annuities : Annuity Due , Finding Future Value

Thanks to all of you who support me on Patreon. You da real mvps! $1 per month helps!! :) https://www.patreon.com/patrickjmt !! Annuities : Annuity Due , Finding Future Value. In this video, we invest a fixed amount at regular intervals in an annuity due. We then find the future value

From playlist Financial Math