Aging, middle class and tech-savvy: global demographic shifts are changing financial risk

Cosimo Pacciani, CRO, European Stability Mechanism, outlines the pressures that are on the welfare and social systems due to aging populations and growing middle classes. Find out more about RiskMinds International at https://goo.gl/Gj8bRf

From playlist Innovation and disruption: Causing ripples in risk

FRM: Risk-adjusted performance ratios

RAPMs are variations of: return per unit of risk. Treynor and Sharpe are similar: both are excess return per unit of risk. Treynor defines risk as systematic risk (beta) and is therefore appropriate to well-diversified portfolios (i.e., into such portfolios idiosyncratic risk is eliminated

From playlist Performance measures

Cosimo Pacciani: Contagion risk and safety nets to widespread crises

At RiskMinds International, Liz MacKean interviews Cosimo Pacciani, CRO at European Stability Mechanism. He discusses strategies to manage contagion risk, and the extent to which Brexit poses a contagion risk in the finance sector. Find out more at https://goo.gl/KVtbtC.

From playlist CRO forum

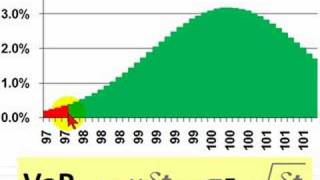

FRM: Parametric value at risk (VaR): Pros & Cons

Here is a quick explanation of parametric value at risk (VaR) as a means to illustrating its strengths/weaknesses. Please note: The essence of parametric VaR is "no data:" while historical data is surely used to select a distribution and calibrate its parameters, a parametric VaR leans on

From playlist Value at Risk (VaR): Introduction

Making Decisions under Model Misspecification & Star-shaped Risk Measures - Maccheroni & Marinacci

Prof. Fabio Maccheroni & Prof. Massimo Marinacci - Making Decisions under Model Misspecification & Star-shaped Risk Measures Making Decisions under Model Misspecification (45min) Authors Simone Cerreia-Vioglio, Lars Peter Hansen, Fabio Maccheroni, Massimo Marinacci Abstract We use de

From playlist Uncertainty and Risk

Financial Markets (ECON 252) The stock market is the information center for the corporate sector. It represents individuals' ownership in publicly-held corporations. Although corporations have a variety of stakeholders, the shareholders of a for-profit corporation are central since the

From playlist Financial Markets (2008) with Robert Shiller

Time Varying Volatility and GARCH in Risk Management

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle In Todays video let's learn abo

From playlist Risk Management

(ML 11.3) Frequentist risk, Bayesian expected loss, and Bayes risk

A simple way to visualize the relationships between the frequentist risk, Bayesian expected loss, and Bayes risk.

From playlist Machine Learning

1. Finance and Insurance as Powerful Forces in Our Economy and Society

Financial Markets (ECON 252) Professor Shiller provides a description of the course, Financial Markets, including administrative details and the topics to be discussed in each lecture. He briefly discusses the importance of studying finance and each key topic. Lecture topics will includ

From playlist Financial Markets (2008) with Robert Shiller

Modigliani, Young Woman in a Shirt

Amedeo Modigliani, Young Woman in a Shirt, 1918, oil on canvas (Albertina, Vienna). Created by Beth Harris and Steven Zucker.

From playlist Expressionism to Pop Art | Art History | Khan Academy

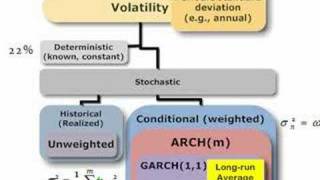

Lots of ways to estimate volatility. In this map, I parse out implied volatility (forward looking) and deterministic (constant) and focus on stochastic volatility: volatility that changes over time, either via (conditional) recent volatility and/or random shocks. For more financial risk vi

From playlist Volatility

FRM: Intro to Credit: Adjusted Exposure

Adjusted Exposure (AE) is a component of credit portfolio expected loss (EL). The adjusted exposure is only the risky portion of the loan asset. It consist of: 1. All outstanding (OS) and 2. Usage given default (UGD) multiplied by commitments. Usage given default (UGD) parameterizes credit

From playlist Credit Risk: Introduction

ARTS: Italian art treasures arrive by ship for show at Royal Academy (1929)

EMPIRE NEWS NEWSREEL (REUTERS) To license this film, visit https://www.britishpathe.com/video/VLVA77CA5QX25BMB0LV00GKNABMGA-ARTS-ITALIAN-ART-TREASURES-ARRIVE-BY-SHIP-FOR-SHOW-AT-ROYAL The "Leonardo da Vinci" ship arrives carrying 14,000,000 pounds worth of art for the Exhibition of Itali

From playlist EMPIRE NEWS NEWSREEL (REUTERS)

1. Introduction and What this Course Will Do for You and Your Purposes

Financial Markets (2011) (ECON 252) Professor Shiller provides a description of the course, including its general theme, the relevant textbooks, as well as the interplay of his course with Professor Geanakoplos's course "Economics 251--Financial Theory." Finance, in his view, is a pillar

From playlist Financial Markets (2011) with Robert Shiller