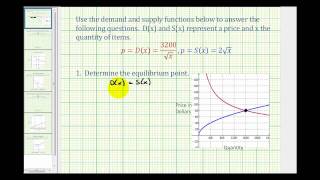

This video shows an example of how to determine the point of equilibrium given the supply and demand functions. Complete Video Library at www.mathispower4u.com

From playlist Business Applications of Integration

Unit 4 - practice problem 3 question

From playlist Courses and Series

http://mathispower4u.wordpress.com/

From playlist Applications of Definite Integration

2. Utilities, Endowments, and Equilibrium

Financial Theory (ECON 251) This lecture explains what an economic model is, and why it allows for counterfactual reasoning and often yields paradoxical conclusions. Typically, equilibrium is defined as the solution to a system of simultaneous equations. The most important economic mode

From playlist Financial Theory with John Geanakoplos

Unit 8 - practice problem 2 solution

From playlist Courses and Series

Twenty second SIAM Activity Group on FME Virtual Talk Series

Join us for a series of online talks on topics related to mathematical finance and engineering and running every two weeks until further notice. The series is organized by the SIAM Activity Group on Financial Mathematics and Engineering. Date: Thursday, October 7, 2021, 1PM-2PM Speaker

From playlist SIAM Activity Group on FME Virtual Talk Series

Combinatorial Markets with Covering Constraints: Algorithms and Applications by Ruta Mehta

Algorithms and Optimization https://www.icts.res.in/discussion-meeting/wao2018 DATES: 02 January 2018 to 03 January 2018 VENUE : Ramanujan Lecture Hall, ICTS Bangalore DESCRIPTION: The goal of this discussion meeting is to bring together leading young researchers in the areas of algori

From playlist Algorithms and Optimization

Nash Equilibriums // How to use Game Theory to render your opponents indifferent

Check out Brilliant ► https://brilliant.org/TreforBazett/ Join for free and the first 200 subscribers get 20% off an annual premium subscription. Thank you to Brilliant for sponsoring this playlist on Game Theory. Game Theory Playlist ► https://www.youtube.com/playlist?list=PLHXZ9OQGMqx

From playlist Game Theory

Ruta Mehta: A Market for Scheduling, with Applications to Cloud Computing

We present a market for allocating and scheduling resources to agents who have specified budgets and need to complete specific tasks. Two important aspects required in this market are: (1) agents need specific amounts of each resource to complete their tasks, and (2) agents would like to c

From playlist HIM Lectures: Trimester Program "Combinatorial Optimization"

ML Tutorial: Adversarial and Competitive Methods in Machine Learning (Amos Storkey)

Machine Learning Tutorial at Imperial College London: Adversarial and Competitive Methods in Machine Learning Amos Storkey (University of Edinburgh) October 28, 2015

From playlist Machine Learning Tutorials

Lecture 17: Existence of Equilibria

MIT 14.04 Intermediate Microeconomic Theory, Fall 2020 Instructor: Prof. Robert Townsend View the complete course: https://ocw.mit.edu/courses/14-04-intermediate-microeconomic-theory-fall-2020/ YouTube Playlist: https://www.youtube.com/watch?v=XSTSfCs74bg&list=PLUl4u3cNGP63wnrKge9vllow3Y2

From playlist MIT 14.04 Intermediate Microeconomic Theory, Fall 2020

How can we understand our complex economy?

Oxford Mathematics Public Lectures: Doyne Farmer - How can we understand our complex economy? We are getting better at predicting things about our environment - the impact of climate change for example. But what about predicting our collective effect on ourselves? We can predict the small

From playlist Oxford Mathematics Public Lectures

Lec 11 | MIT 14.01SC Principles of Microeconomics

Lecture 11: Competition II Instructor: Jon Gruber, 14.01 students View the complete course: http://ocw.mit.edu/14-01SCF10 License: Creative Commons BY-NC-SA More information at http://ocw.mit.edu/terms More courses at http://ocw.mit.edu

From playlist MIT 14.01SC Principles of Microeconomics

From playlist Courses and Series

From playlist Courses and Series

Unit 5 - practice problem 1 question

From playlist Courses and Series