Understanding the Deflection of Beams

Sign up for Brilliant at https://brilliant.org/efficientengineer/, and start your journey towards calculus mastery! The first 200 people to sign up using this link will get 20% off the annual premium subscription! In this video I take a look at five methods that can be used to predict how

From playlist Mechanics of Materials / Strength of Materials

Fixed Income: Analytical Convexity; aka, modified convexity (FRM T4-41)

In this video, I will show you how to calculate modified convexity by matching the modified convexity that Tuckman shows in Table 4.6 in Chapter 4 of his book, Fixed Income Securities. 💡 Discuss this video here in our forum: https://trtl.bz/2YBEHeB. 📗 You can find Tuckman's Fixed Income

From playlist Valuation and RIsk Models (FRM Topic 4)

Fixed Income: Impact of Yield and Coupon on Duration and DV01 (FRM T4-39)

The previous videos in this playlist have illustrated how we calculate the two most popular measures of single-factor interest rate sensitivity, that is duration and dv01, also called price value of the basis point. Now, knowing how these calculations work we will apply them to understand

From playlist Valuation and RIsk Models (FRM Topic 4)

Fixed Income: Simple bond illustrating all three durations (effective, mod, Mac) (FRM T4-36)

Macaulay duration is the bond's weighted average maturity (where the weights are each cash flow's present value as a percent of the bond's price; in this example, the bond's Macaulay duration is 2.8543 years. Modified duration is the true (best) measure of interest rate risk; in this examp

From playlist Valuation and RIsk Models (FRM Topic 4)

Commutative algebra 62: Cohen Macaulay local rings

This lecture is part of an online course on commutative algebra, following the book "Commutative algebra with a view toward algebraic geometry" by David Eisenbud. We define Cohen-Macaulay local rings, and give some examples of local rings that are Cohen-Macaualy and some examples that are

From playlist Commutative algebra

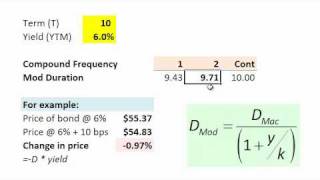

Modified duration of zero-coupond bond (FRM practice question)

A zero-coupon bond with maturity of ten (10) years has a 6% bond-equivalent yield (semi-annual compounding). What is the bond's modified duration?

From playlist Bonds: Sensitivities

Fixed Income: Duration and Convexity Summary (FRM T4-42)

In this playlist, I've already recorded at least ten videos on duration and convexity which are the two most common measures of single-factor interest rate risk. So, in this video, we wrap it up in one simple explanation that tries to illustrate both duration and convexity and how we apply

From playlist Valuation and RIsk Models (FRM Topic 4)

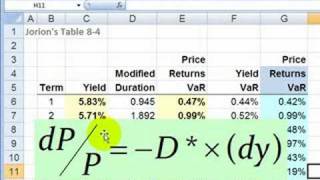

FRM: Bond returns value at risk (VaR) as bond risk

Bond risk can be measured by "price returns value at risk (VaR)" where the price returns VaR is linked to yield VaR with duration. For more financial risk videos, visit our website! http://www.bionicturtle.com

From playlist Value at Risk (VaR): VaR Mapping

Alfred Noël - Molien Series and a Recent Theorem of Kostant

Research lecture at the Worldwide Center of Mathematics

From playlist Center of Math Research: the Worldwide Lecture Seminar Series

Reflections: Science and Religion, Natural and Unnatural

Dwight H. Terry Lectureship October 26, 2006 Reflections: Science and Religion, Natural and Unnatural Barbara Herrnstein Smith is Braxton Craven Professor of Comparative Literature and English and director of the Center for Interdisciplinary Studies in Science and Cultural Theory at

From playlist Terry Lectures