Capital asset pricing model (CAPM, FRM T1-9)

The CAPM is a ex ante single-factor model where the single-factor is the market's excess return: it says that we should expect an excess return that is proportional to the stock's beta, which is the stock's exposure to market's excess return, as measured by the stock's beta. Beta can be re

From playlist Risk Foundations (FRM Topic 1)

Applied Portfolio Management - Video 4 - Fixed Income Asset Management

All slides are available on my Patreon page: https://www.patreon.com/PatrickBoyleOnFinance Fixed income refers to any type of investment under which the borrower or issuer is obliged to make payments of a fixed amount on a fixed schedule. For example, the borrower may have to pay interest

From playlist Applied Portfolio Management

This video explains the math behind investing in mutual funds. It discusses the value of a mutual fund's annual performance and the value of investing long term. A equity mutual fund is a financial vehicle that invests in a variety of stocks. Thus a mutual fund is a passive way for an i

From playlist Stocks and Bonds

Two-asset portfolio volatility

The very traditional (mean-variance) two asset portfolio volatility is largely a function of asset correlation/covariance.

From playlist Intro to Quant Finance

Pricing Options Using the Binomial Tree (Risk Neutral Valuation Approach)

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle In finance, the binomial option

From playlist Class 3: Pricing Financial Options

Financial Markets (2011) (ECON 252) Professor Shiller characterizes investment banking by contrasting it to consulting, commercial banking, and securities trading. Then, in order to see the essence of investment banking, he reviews some of the principles that John Whitehead, the former c

From playlist Financial Markets (2011) with Robert Shiller

Asset Allocation Strategies for the New Decade

Martin Leibowitz, Managing Director, Morgan Stanley; Robert Litterman, Retired Partner, Goldman Sachs & Co.; and John L. (Launny) Steffens, Founder, Spring Mountain Capital June 17, 2010 The Einstein Legacy Society recognizes those friends of the Institute who have made a planned gift or

From playlist Einstein Legacy Society

7. Behavioral Finance: The Role of Psychology

Financial Markets (ECON 252) Behavioral Finance is a relatively recent revolution in finance that applies insights from all of the social sciences to finance. New decision-making models incorporate psychology and sociology, among other disciplines, to explain economic and financial phen

From playlist Financial Markets (2008) with Robert Shiller

Financial Markets (ECON 252) The stock market is the information center for the corporate sector. It represents individuals' ownership in publicly-held corporations. Although corporations have a variety of stakeholders, the shareholders of a for-profit corporation are central since the

From playlist Financial Markets (2008) with Robert Shiller

MIT MAS.S62 Cryptocurrency Engineering and Design, Spring 2018 Instructor: Neha Narula View the complete course: https://ocw.mit.edu/MAS-S62S18 YouTube Playlist: https://www.youtube.com/playlist?list=PLUl4u3cNGP61KHzhg3JIJdK08JLSlcLId zkLedger, a private, auditable transaction ledger for

From playlist MIT MAS.S62 Cryptocurrency Engineering and Design, Spring 2018

WECode 2016 Lightning Talk with Jenny Li (Goldman Sachs)

About WECode: WECode (Women Engineers Code) is the largest student-run Women in Computer Science conference, held at Harvard University each February. Our mission is to expand the skills, network, and community of technical women worldwide. We bring together women over the course of two a

From playlist WECode 2016

21. Guest Lecture by Paolo Zanonni, Part I

Capitalism: Success, Crisis and Reform (PLSC 270) Guest speaker Paolo Zanonni, partner at Goldman Sachs, discusses the firm's transition from a straight partnership to a hybrid partnership/joint stock corporation. The impetus for the transition was obtain the advantages of the joint sto

From playlist Capitalism: Success, Crisis and Reform with Douglas W. Rae

14. Guest Speaker Maurice "Hank" Greenberg

Financial Markets (2011) (ECON 252) This is a guest lecture by Maurice "Hank" Greenberg, former Chief Executive Officer at American International Group. Mr. Greenberg starts his lecture with reflections on his time in the U.S. Army during World War II and the Korean War as well as on his

From playlist Financial Markets (2011) with Robert Shiller

21. Post Trade Clearing, Settlement & Processing

MIT 15.S12 Blockchain and Money, Fall 2018 Instructor: Prof. Gary Gensler View the complete course: https://ocw.mit.edu/15-S12F18 YouTube Playlist: https://www.youtube.com/playlist?list=PLUl4u3cNGP63UUkfL0onkxF6MYgVa04Fn Prof. Gensler leads a discussion on clearing and settlement systems,

From playlist MIT 15.S12 Blockchain and Money, Fall 2018

Applied Portfolio Management Private Equity | Leveraged Buyouts | Venture Capital

All slides are available on my Patreon page: https://www.patreon.com/PatrickBoyleOnFinance In todays Applied Portfolio Management class we learn about private equity, venture capital, growth capital funds and venture capital. We learn about fund structures, risk and historic returns. So

From playlist Applied Portfolio Management

4. Portfolio Diversification and Supporting Financial Institutions (CAPM Model)

Financial Markets (ECON 252) Portfolio diversification is the most fundamental concept of risk management. The allocation of financial resources in stocks, bonds, riskless, assets, oil and other assets determine the expected return and risk of a portfolio. Taking account of covariances

From playlist Financial Markets (2008) with Robert Shiller

22. Guest Lecture by Paolo Zanonni, Part II

Capitalism: Success, Crisis and Reform (PLSC 270) Guest speaker Paolo Zanonni, partner at Goldman Sachs, explains a major deal in the European utilities market. Enel, a major European utility, attempted to totally transform its position by expanding into the Spanish market and acquiring

From playlist Capitalism: Success, Crisis and Reform with Douglas W. Rae

Frictions in subprime securitization

In subprime securitization, seven frictions are identified, but the key frictions are the five represented by the red line that runs from friction #1 (borrower and originator) to friction #6 (the principal-agent problem between investor and asset manager). The essential problem (though sev

From playlist Credit Risk: Securitization

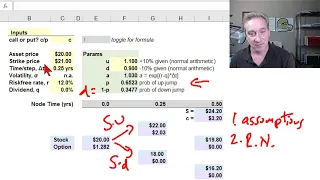

Introduction to binomial option pricing model: two-step (FRM T4-6)

[my xls is here https://trtl.bz/2AruFiH] The binomial option pricing model needs: 1. A set of assumptions similar but not identical to those found in Black-Scholes; 2. A framework; i.e., risk-neutral valuation which allows us to infer the probability of an up-jump; 3. An assumption about a

From playlist Valuation and RIsk Models (FRM Topic 4)