From playlist Courses and Series

From playlist COMP0168 (2020/21)

The Generalized Likelihood Ratio Test

http://AllSignalProcessing.com for more great signal processing content, including concept/screenshot files, quizzes, MATLAB and data files. There is no universally optimal test strategy for composite hypotheses (unknown parameters in the pdfs). The generalized likelihood ratio test (GLRT

From playlist Estimation and Detection Theory

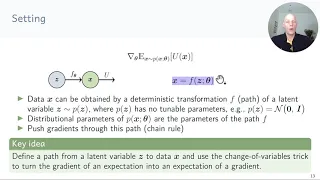

12 Stochastic Gradient Estimators

Slides and more information: https://mml-book.github.io/slopes-expectations.html

From playlist There and Back Again: A Tale of Slopes and Expectations (NeurIPS-2020 Tutorial)

Statistical Analysis Spreadsheet (1 of 3: Calculating expected values)

More resources available at www.misterwootube.com

From playlist Probability and Discrete Probability Distributions

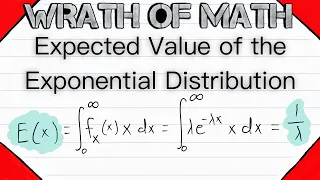

Expected Value of the Exponential Distribution | Exponential Random Variables, Probability Theory

What is the expected value of the exponential distribution and how do we find it? In today's video we will prove the expected value of the exponential distribution using the probability density function and the definition of the expected value for a continuous random variable. It's gonna b

From playlist Probability Theory

The normal distribution | Probability and Statistics | NJ Wildberger

In this final lecture in this short introduction to Probability and Statistics, we introduce perhaps the most important probability distibution: the normal distribution, also known as the `bell-curve'. Its role is clarified by the Central Limit theorem, a key result in Statistics, that sta

From playlist Probability and Statistics: an introduction

Unit 2 - consumer demand part 4

From playlist Courses and Series

Paolo Guasoni, Lesson II - 19 december 2017

QUANTITATIVE FINANCE SEMINARS @ SNS PROF. PAOLO GUASONI TOPICS IN PORTFOLIO CHOICE

From playlist Quantitative Finance Seminar @ SNS

“Choice Modeling and Assortment Optimization” - Session I - Prof. Huseyin Topaloglu

This module overviews static and dynamic assortment optimization problems. We start with an introduction to discrete choice modeling and discuss estimation issues when fitting a choice model to observed sales histories. Following this introduction, we discuss static and dynamic assortment

From playlist Thematic Program on Stochastic Modeling: A Focus on Pricing & Revenue Management

Eliezer Yudkowsky – AI Alignment: Why It's Hard, and Where to Start

On May 5, 2016, Eliezer Yudkowsky gave a talk at Stanford University for the 26th Annual Symbolic Systems Distinguished Speaker series (https://symsys.stanford.edu/viewing/event/26580). Eliezer is a senior research fellow at the Machine Intelligence Research Institute, a research nonprofi

From playlist Machine Learning Shorts

AI That Doesn't Try Too Hard - Maximizers and Satisficers

Powerful AI systems can be dangerous in part because they pursue their goals as strongly as they can. Perhaps it would be safer to have systems that don't aim for perfection, and stop at 'good enough'. How could we build something like that? Generating Fake YouTube comments with GPT-2: ht

From playlist Technical

Paolo Guasoni, Lesson I - 18 december 2017

QUANTITATIVE FINANCE SEMINARS @ SNS PROF. PAOLO GUASONI TOPICS IN PORTFOLIO CHOICE

From playlist Quantitative Finance Seminar @ SNS

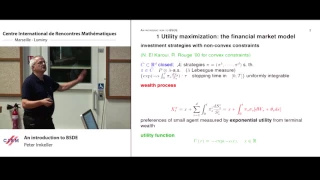

Peter Imkeller: An introduction to BSDE

Abstract: Backward stochastic differential equations have been a very successful and active tool for stochastic finance and insurance for some decades. More generally they serve as a central method in applications of control theory in many areas. We introduce BSDE by looking at a simple ut

From playlist Probability and Statistics

22. Risk Aversion and the Capital Asset Pricing Theorem

Financial Theory (ECON 251) Until now we have ignored risk aversion. The Bernoulli brothers were the first to suggest a tractable way of representing risk aversion. They pointed out that an explanation of the St. Petersburg paradox might be that people care about expected utility inste

From playlist Financial Theory with John Geanakoplos

Multivariate Portfolio Choice via Quantiles

SIAM Activity Group on FME Virtual Talk Series Join us for a series of online talks on topics related to mathematical finance and engineering and running every two weeks until further notice. The series is organized by the SIAM Activity Group on Financial Mathematics and Engineering. Spea

From playlist SIAM Activity Group on FME Virtual Talk Series

Unit 2 - consumer surplus part 2

From playlist Courses and Series

Ellen Vitercik: "How much data is sufficient to learn high-performing algorithms?"

Deep Learning and Combinatorial Optimization 2021 "How much data is sufficient to learn high-performing algorithms?" Ellen Vitercik - Carnegie Mellon University Abstract: Algorithms often have tunable parameters that have a considerable impact on their runtime and solution quality. A gro

From playlist Deep Learning and Combinatorial Optimization 2021