What are Real Options? - Real Options Valuation Method For Capital Budgeting Decisions

Real options valuation, also often termed real options analysis, applies option valuation techniques to capital budgeting decisions. These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our

From playlist Class 5 - Options Wrap Up

Put call parity derives from the idea we can have two portfolios (one with an option, the other with a put) that have identical payoffs regardless of what happens to the stock. This gives a way to link the value of a call option with a put option. For more financial risk videos, visit our

From playlist Derivatives: Option Pricing

Nash Equilibriums // How to use Game Theory to render your opponents indifferent

Check out Brilliant ► https://brilliant.org/TreforBazett/ Join for free and the first 200 subscribers get 20% off an annual premium subscription. Thank you to Brilliant for sponsoring this playlist on Game Theory. Game Theory Playlist ► https://www.youtube.com/playlist?list=PLHXZ9OQGMqx

From playlist Game Theory

Pricing Options Using the Binomial Tree (Risk Neutral Valuation Approach)

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle In finance, the binomial option

From playlist Class 3: Pricing Financial Options

Introduction to binomial option pricing model: two-step (FRM T4-6)

[my xls is here https://trtl.bz/2AruFiH] The binomial option pricing model needs: 1. A set of assumptions similar but not identical to those found in Black-Scholes; 2. A framework; i.e., risk-neutral valuation which allows us to infer the probability of an up-jump; 3. An assumption about a

From playlist Valuation and RIsk Models (FRM Topic 4)

Financial Option Theory with Mathematica -- Volatility, and direct solution of PDEs

This is my third session of my track about Financial Option Theory with Mathematica. I first develop two methods to compute historical volatility of a stock. Next I do the same for an estimate of the historical appreciation rate. I then come to the very important topic of the implied volat

From playlist Financial Options Theory with Mathematica

TEEB for Business-Biodiversity Impacts and Dependencies: TEEB @ Yale

Why are companies interested in biodiversity? What industries are most responsible for and/or vulnerable to biodiversity loss?

From playlist TEEB @ Yale

Lookback options are often used for commodities, as a lookback call is a way to buy the asset at the lowest price and a lookback put is a way to sell the asset at the highest price. Although the pricing formulas assuming continuous asset price paths, the frequency of measuring (observing)

From playlist Derivatives: Exotic Options

Volatility Arbitrage - How does it work? - Options Trading Lessons

What is Volatility Arbitrage? Volatility arbitrage is a trading strategy that attempts to profit from the difference between the forecasted price-volatility of an asset, like a stock, and the implied volatility of options on that asset. These classes are all based on the book Trading and

From playlist Class 4 The Greeks & Dynamic Hedging

Valuation Approaches & Paradigms Part 2: TEEB@YALE

Valuation approaches & paradigms; Biophysical approaches; the Total Economic Value (TEV) framework & its various valuation methods ; acknowledging uncertainties in valuation ; Insurance value and Resilience ; Quasi-Option Values ; Valuation across Stakeholders ; Valuation in developing cou

From playlist TEEB @ Yale

Valuation Approaches & Paradigms Part 1: TEEB@YALE

Valuation approaches & paradigms; Biophysical approaches; the Total Economic Value (TEV) framework & its various valuation methods; acknowledging uncertainties in valuation ; Insurance value and Resilience ; Quasi-Option Values ; Valuation across Stakeholders ; Valuation in developing coun

From playlist TEEB @ Yale

Here is an spreadsheet example of pricing a European call option on a stock index (e.g., Dow Jones Utility) with a two step binomial. There are two basic process steps: 1. Build forward the "tree" of asset prices, 2. Then backward induction: value the option at each node as the PROBABILITY

From playlist Derivatives: Option Pricing

Pricing Options - Revision Lecture

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle

From playlist Revision Lectures

Valuation Approaches & Paradigms Part 3: TEEB@YALE

Valuation approaches & paradigms; Biophysical approaches; the Total Economic Value (TEV) framework & its various valuation methods; acknowledging uncertainties in valuation ; Insurance value and Resilience ; Quasi-Option Values ; Valuation across Stakeholders ; Valuation in developing coun

From playlist TEEB @ Yale

Swaps and Credit Derivatives - Revision Lecture

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle

From playlist Revision Lectures

Ngoc Mai Tran: Tropical solutions to hard problems in auction theory and neural networks, lecture I

Tropical mathematics is mathematics done in the min-plus (or max-plus) algebra. The power of tropical mathematics comes from two key ideas: (a) tropical objects are limits of classical ones, and (b) the geometry of tropical objects is polyhedral. In this course, I’ll demonstrate how these

From playlist Summer School on modern directions in discrete optimization

Applied Portfolio Management - Class 7 - Hedge Fund Strategies - How Hedge Funds Invest

All slides are available on my Patreon page: https://www.patreon.com/PatrickBoyleOnFinance Applied Portfolio Management - How Hedge Funds Invest. In todays class we learn what a hedge fund is, we learn why people invest in them, and how hedge funds and other alternative investments might

From playlist Applied Portfolio Management

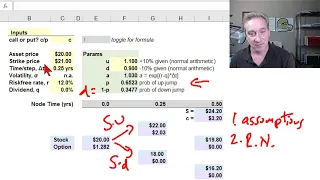

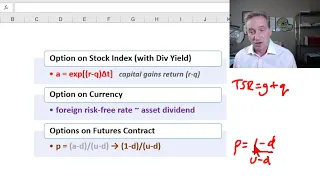

Binomial option pricing model for equity index, currencies, and futures options (FRM T4-9)

[here is my xls https://trtl.bz/2AZLCkA] Using a three-step binomial to price "options on other assets" (Hull 13.11 10th edition): equity index option, currency options and futures options (aka, options on futures contracts). The key difference is the calculation of p = probability of an u

From playlist Valuation and RIsk Models (FRM Topic 4)

Lecture 11 - Risk-Neutral Valuation

This is Lecture 11 of the COMP510 (Computational Finance) course taught by Professor Steven Skiena [http://www.cs.sunysb.edu/~skiena/] at Hong Kong University of Science and Technology in 2008. The lecture slides are available at: http://www.algorithm.cs.sunysb.edu/computationalfinance/pd

From playlist COMP510 - Computational Finance - 2007 HKUST