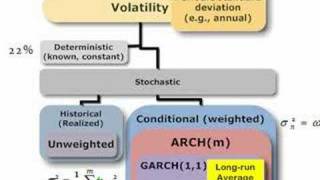

Lots of ways to estimate volatility. In this map, I parse out implied volatility (forward looking) and deterministic (constant) and focus on stochastic volatility: volatility that changes over time, either via (conditional) recent volatility and/or random shocks. For more financial risk vi

From playlist Volatility

Volatility Trading - Call and Put Options - Trading Tutorial

These classes are all based on the book Derivatives For The Trading Floor, available on Amazon at this link. https://amzn.to/3GdLi2s Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle What is volatility trading? Volatility

From playlist Class 4 The Greeks & Dynamic Hedging

FRM: Forecast volatility with GARCH(1,1)

We can forecast volatility with GARCH(1,1). The key parameter is persistence (alpha + beta): high persistence implies slow decay toward the long run average. For more financial risk videos, visit our website! http://www.bionicturtle.com

From playlist Volatility

What are Volatility Swaps? Financial Derivatives - Trading Volatility

In todays class we learn about what a volatility swap is. These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https:/

From playlist The Term Structure of Volatility

Risk Management Lesson 4A: Volatility

First part of Lesson 4. Topics: - Definitions of volatility - Basic assumptions (do they hold?) - Arch and G-arch models (brief overview)

From playlist Risk Management

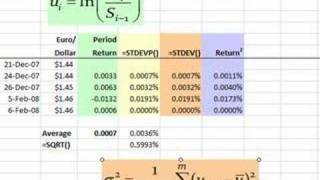

FRM: How to calculate (simple) historical volatlity

Historical daily volatility is the square root of the daily variance estimate. If we assume 1. mean return = 0 and 2. MLE rather than unbiased estimate, then daily variance is AVERAGE SQUARED RETURN. For more financial risk videos, visit our website! http://www.bionicturtle.com

From playlist Volatility

What is a Forward Contract? In finance, a forward contract or simply a forward is a non-standardized contract between two parties to buy or to sell an asset at a specified future time at a price agreed upon today. The party agreeing to buy the underlying asset in the future assumes a long

From playlist Class 1 Futures & Forwards

Time Varying Volatility and GARCH in Risk Management

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle In Todays video let's learn abo

From playlist Risk Management

FRM: Volatility: Moving Average Approaches

Within stochastic volatility, moving average is the simplest approach. It simply calculates volatility as the unweighted standard deviation of a window of X trading days. Here I show the three "flavors:" population variance (volatility = SQRT[variance]), sample, and simple. For more financ

From playlist Volatility

Forecast volatility with GARCH(1,1) (FRM T2-24)

[my xls is here https://trtl.bz/2yGdnjv] The GARCH(1,1) volatility forecast is largely a function of the first term omega, ω = γ*V(L), which itself is the product of a rate of reversion, γ, and a reversion level, V(L); aka, long-run or unconditional variance. Discuss this video here in our

From playlist Quantitative Analysis (FRM Topic 2)

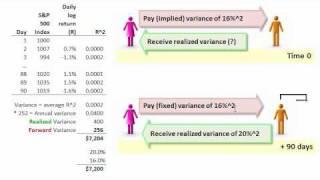

A variance swap can be used to hedge tail risk. One counterparty (Sally the trader, in this example) pays a forward (fixed) variance in exchange for a future, REALIZED variance. So she is "long volatility" and will profit if the realized variance is greater than expected. The advantage of

From playlist Derivatives: Exotic Options

The VIX Index and US Elections | Trump Biden 2020 | VIX Futures | Risk Management

As the U.S. stock market continues to rally to record highs, the attention of many investors is turning toward November’s elections as a source of risk. Hedging against that potential market volatility does not come cheap. In fact, it’s currently the most-expensive event risk on record bas

From playlist The Term Structure of Volatility

Financial Option Theory with Mathematica -- Volatility, and direct solution of PDEs

This is my third session of my track about Financial Option Theory with Mathematica. I first develop two methods to compute historical volatility of a stock. Next I do the same for an estimate of the historical appreciation rate. I then come to the very important topic of the implied volat

From playlist Financial Options Theory with Mathematica

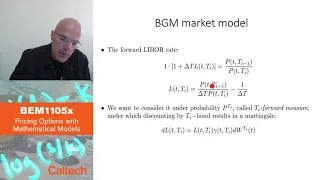

10 9 Forward rates models Part 3

BEM1105x Course Playlist - https://www.youtube.com/playlist?list=PL8_xPU5epJdfCxbRzxuchTfgOH1I2Ibht Produced in association with Caltech Academic Media Technologies. ©2020 California Institute of Technology

From playlist BEM1105x Course - Prof. Jakša Cvitanić

10 8 Forward rates models Part 2

BEM1105x Course Playlist - https://www.youtube.com/playlist?list=PL8_xPU5epJdfCxbRzxuchTfgOH1I2Ibht Produced in association with Caltech Academic Media Technologies. ©2020 California Institute of Technology

From playlist BEM1105x Course - Prof. Jakša Cvitanić

Risk Management of Option Books with Arbitrage-Free Neural-SDE Market Models (SIAM FME)

SIAM Activity Group on FME Virtual Talk Series Join us for a series of online talks on topics related to mathematical finance and engineering and running every two weeks until further notice. The series is organized by the SIAM Activity Group on Financial Mathematics and Engineering. Spe

From playlist SIAM Activity Group on FME Virtual Talk Series

Convexity adjustment for Eurodollar futures

A key difference between a futures contract and a forward contract is daily settlement: the instrument is daily marked-to-market. If the value of the futures increases, this creates excess margin cash; if value declines, there will be a margin call (when the maintenance level is reached).

From playlist Derivatives: Interest Rate Derivatives

FRM: GARCH(1,1) to estimate volatility

GARCH(1,1) estimates volatility in a similar way to EWMA (i.e., by conditioning on new information) EXCEPT it adds a term for mean reversion: it says the series is "sticky" or somewhat persistent to a long-run average. For more financial risk videos, visit our website! http://www.bionictur

From playlist Volatility