Floating and Fixed Exchange Rates- Macroeconomics

Float it or fix it? Mr. Clifford expalins the difference between floating and fixed exchange rates and how countries peg the value of their currency to another currency. Make sure to watch this video first: https://www.youtube.com/watch?v=9DVYVfI81R8

From playlist Macro Unit 6: Open Economy- International Trade and Finance

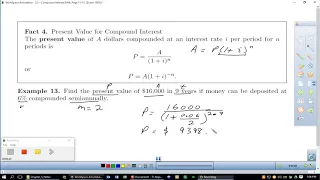

Effective Interest Rate (Effective Yield)

This video shows how to derive the effective interest rate formula for compounded and continuous interest. It also provides two examples on how to calculate effective interest rate. Site: http://mathispower4u.com Search: http://mathispower4u.wordpress.com

From playlist Finance: Simple and Compounded Interest

Estimating Credit Card Interest 3

From playlist Personal Finance

Understanding Simple Interest and Compound Interest

Thanks to all of you who support me on Patreon. You da real mvps! $1 per month helps!! :) https://www.patreon.com/patrickjmt !! Understanding Simple Interest and Compound Interest - In this video I try to make clear the difference between simple interest and compound interest!

From playlist Financial Math

From playlist MATH 1324: Finite Mathematics

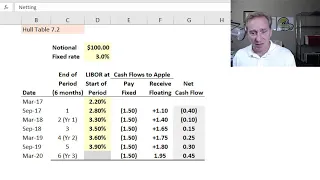

Plain vanilla interest rate swap (T3-30)

[here in my xls https://trtl.bz/2QBc5et] The "plain vanilla" interest rate swap is the common interest rate derivative: one counterparty, in this example Apple (who is the "fixed-rate payer") agrees to pay cash flows equal to interest at a predetermined FIXED rate on a notional amount (in

From playlist Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

10. Debt Markets: Term Structure

Financial Markets (ECON 252) The markets for debt, both public and private far exceed the entire stock market in value and importance. The U.S. Treasury issues debt of various maturities through auctions, which are open only to authorized buyers. Corporations issue debt with investment

From playlist Financial Markets (2008) with Robert Shiller

Simple Interest - Determine Account Balance (Monthly Interest)

This video explains how to solve a problem using the simple interest formula. http://mathispower4u.com

From playlist Percent Applications

Swaps and Credit Derivatives - Revision Lecture

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle

From playlist Revision Lectures

Valuation of plain-vanilla interest rate swap (T3-32)

[here is my XLS https://trtl.bz/2Q4XFCh] I breakdown the valuation of an interest rate swap into three steps: 1. The assumptions, which includes understanding the TIMELINE; e.g., we are valuing the stop at some point after origination and it has some remaining life (in this case 15 months)

From playlist Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

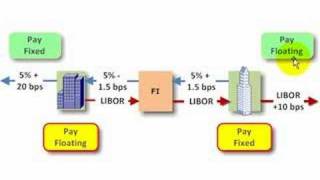

This illustrates how an interest rate swap can transform a floating-rate obligation into a fixed-rate obligation and vice-versa. For more great financial risk management videos, visit the Bionic Turtle website! http://www.bionicturtle.com

From playlist Derivatives: Interest Rate Derivatives

FRM: How to value an interest rate swap

At inception, the value of the swap is zero or nearly zero. Subsequently, the value of the swap will differ from zero. Under this approach, we simply treat the swap as two bonds: a fixed-coupon bond and a floating-coupon bond. The value of the swap is difference between the two. For more f

From playlist Derivatives: Interest Rate Derivatives

Financial Derivatives - Lecture 7 - Forward Rate Agreements & Swaps

These full length lectures are being provided for students who are unable to attend live university lectures due to the public health issues associated with Covid 19. I will return to my standard YouTube video format shortly. Buy The Book Here: https://amzn.to/2Qdj9zu Visit our website.

From playlist Full Financial Derivatives Lectures

FRM: Interest rate swap (IRS) valuation: as two bonds

This video illustrates the valuation of an interest rate swap as two bonds. For more information on interest rate swap (IRS), visit Bionic Turtle at https://www.bionicturtle.com.

From playlist Swaps

In todays video we will learn the two methods for pricing interest rate swaps. These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on t

From playlist Swaps

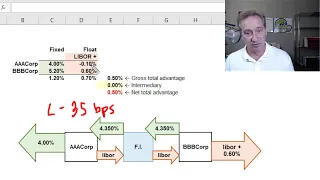

Comparative advantage in an interest rate swap (FRM T3-31)

[my xls is here https://trtl.bz/2DceGc6] AAACorp has a comparative advantage in fixed-rate markets, but BBBCorp has a comparative advantage in floating-rate markets (even as it pays more everwhere!). The difference in spreads (in this case, the difference is 0.50% = 1.20% - 0.70%) is the g

From playlist Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

What are Negative Interest Rates? (And How do They Work?)

Negative interest rates mean you get paid to borrow money. Sound too good to be true? It is. Get a free stock with WeBull: https://bit.ly/2tBxZYv Get a free stock with Robinhood: https://bit.ly/3cB9Xxa In most countries around the world, there’s a central bank that has a number of tools

From playlist Concerning Finance

What are Dividend Swaps, commodity swaps, equity swaps?

In todays video we will learn about Dividend Swaps, Commodity Swaps and Equity Swaps. These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patri

From playlist Swaps