FRM: Forecast volatility with GARCH(1,1)

We can forecast volatility with GARCH(1,1). The key parameter is persistence (alpha + beta): high persistence implies slow decay toward the long run average. For more financial risk videos, visit our website! http://www.bionicturtle.com

From playlist Volatility

Two-asset portfolio volatility

The very traditional (mean-variance) two asset portfolio volatility is largely a function of asset correlation/covariance.

From playlist Intro to Quant Finance

Sylvia Frühwirth-Schnatter: Bayesian econometrics in the Big Data Era

Abstract: Data mining methods based on finite mixture models are quite common in many areas of applied science, such as marketing, to segment data and to identify subgroups with specific features. Recent work shows that these methods are also useful in micro econometrics to analyze the beh

From playlist Probability and Statistics

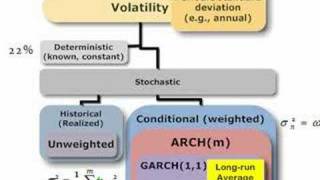

Lots of ways to estimate volatility. In this map, I parse out implied volatility (forward looking) and deterministic (constant) and focus on stochastic volatility: volatility that changes over time, either via (conditional) recent volatility and/or random shocks. For more financial risk vi

From playlist Volatility

Network Analysis. Lecture 3. Random graphs.

Erdos-Reni random graph model. Poisson and Bernulli distributions. Distribution of node degrees. Phase transition, gigantic connected component. Diameter and cluster coefficient. Configuration model Lecture slides: http://www.leonidzhukov.net/hse/2015/networks/lectures/lecture3.pdf

From playlist Structural Analysis and Visualization of Networks.

Statistics: Introduction to the Shape of a Distribution of a Variable

This video introduces some of the more common shapes of distributions http://mathispower4u.com

From playlist Statistics: Describing Data

Promoting global stability in data-driven models of quadratic nonlinear dynamics - Trapping SINDy

System identification methods attempt to discover physical models directly from a dataset of measurements, but often there are no guarantees that the resulting models are stable. This video abstract summarizes our recent work that builds in a notion of long-term boundedness (or global stab

From playlist Research Abstracts from Brunton Lab

The Term Structure of Volatility and the Volatility Surface

Today we will learn about the volatility Surface. These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter

From playlist The Term Structure of Volatility

Financial Derivatives - Lecture 8 - Monte Carlo Method & Risk Management

These full length lectures are being provided for students who are unable to attend live university lectures due to the public health issues associated with Covid 19. I will return to my standard YouTube video format shortly. Buy The Book Here: https://amzn.to/2Qdj9zu Visit our website.

From playlist Full Financial Derivatives Lectures

Risk Management Lesson 4A: Volatility

First part of Lesson 4. Topics: - Definitions of volatility - Basic assumptions (do they hold?) - Arch and G-arch models (brief overview)

From playlist Risk Management

Welcome to Quantitative Risk Management (QRM). In this lesson, we play with R to deal with VaR and ES. We show how to compute them empirically, but also in the case of normality. We then show that normality tends to underestimate tail risk, as observable in actual financial data. The pdf

From playlist Quantitative Risk Management

Milad Bakhshizadeh (Columbia) -- Sharp Concentration Resultsfor Heavy-Tailed Distributions

We obtain concentration and large deviation for the sums of independent and identically distributed random variables with heavy-tailed distributions. Our main theorem can not only recover some of the existing results, such as the concentration of the sum of subWeibull random variables, but

From playlist Northeastern Probability Seminar 2020

QRM 8-2: (G)ARCH Models for volatility

Welcome to Quantitative Risk Management (QRM) In the second part of Lesson 8, we cover the basics of volatility modelling, because markets are heteroschedastic! We will speak about Arch and Garch models, focusing on some relevant but often ignored consequences of these models. For exampl

From playlist Quantitative Risk Management

A conversation between Nassim Nicholas Taleb and Stephen Wolfram at the Wolfram Summer School 2021

Stephen Wolfram plays the role of Salonnière in this new, on-going series of intellectual explorations with special guests. Watch all of the conversations here: https://wolfr.am/youtube-sw-conversations Follow us on our official social media channels. Twitter: https://twitter.com/Wolfra

From playlist Conversations with Special Guests

QRM 8-3: R lesson on extremal index, records and Garch

Welcome to Quantitative Risk Management (QRM). In this lesson we use R Studio to study the extremal index and Garch models. We will also discuss the use of "records," to understand if our data are i.i.d. or not, and if they might satisfy the so-called D conditions. R notebook: https://ww

From playlist Quantitative Risk Management

How do you calculate value at risk? Two ways of calculating VaR

In todays video we learn how to calculate VaR or Value at Risk. Buy The Book Here: https://amzn.to/37HIdEB Follow Patrick on Twitter Here: https://twitter.com/PatrickEBoyle What is VAR? The most popular and traditional measure of risk is volatility. The main problem with volatility, how

From playlist Risk Management

Lecture 10 - Price Distributions

This is Lecture 10 of the COMP510 (Computational Finance) course taught by Professor Steven Skiena [http://www.cs.sunysb.edu/~skiena/] at Hong Kong University of Science and Technology in 2008. The lecture slides are available at: http://www.algorithm.cs.sunysb.edu/computationalfinance/pd

From playlist COMP510 - Computational Finance - 2007 HKUST

The Volatility Smile - Options Trading Lessons

The volatility smile is a real-life pattern that is observed when different strikes of option, with the same underlying and same expiration date are plotted on a graph. These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. htt

From playlist The Term Structure of Volatility

Risk Management Lesson 4B: Volatility (second part) and Coherent Risk Measures

This is the second half of Lesson 4. Topics: - Exercise about volatility modeling with G-arch - Coherent risk measures - Are the variance and the standard deviation coherent? A useful document for you is available here: https://www.dropbox.com/s/6pdygf0bw6bcce1/coherence.pdf

From playlist Risk Management

Solving BCBS-185 with Machine Learning

The Basel directive, BCBS-185, outlines sound practices for back-testing counterparty risk models to ensure they are effective. Here, Peter Zeitsch, Solution Architecht at Calypso Technology, argued that it essentially reduces to one tricky requirement: capturing the ‘black-swans’ or jumps

From playlist Innovation and disruption: Causing ripples in risk