Evaluating Time Series Models : Time Series Talk

How do we evaluate our time series models? How can we tell if one model is better than another?

From playlist Time Series Analysis

Statistics Lecture 8.2: An Introduction to Hypothesis Testing

https://www.patreon.com/ProfessorLeonard Statistics Lecture 8.2: An Introduction to Hypothesis Testing

From playlist Statistics (Full Length Videos)

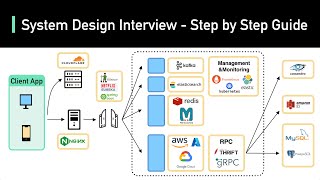

System Design Interview: A Step-By-Step Guide

Learn something new every week by subscribing to our newsletter: https://bit.ly/3tfAlYD Checkout our bestselling System Design Interview books: Volume 1: https://amzn.to/3Ou7gkd Volume 2: https://amzn.to/3HqGozy ABOUT US: Covering topics and trends in large-scale system design, from th

From playlist System Design Interview

This latest video provides 3x top tips to consider when going for interviews. You may be surprised at what you forget.

From playlist Job Interviews

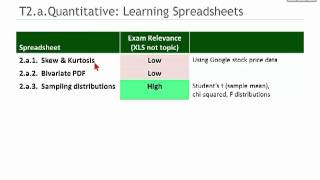

FRM Part 1 Focus Review: 2nd of 8 (Quantitative)

This is a sample of our 2012 FRM Part 1 Focus Review: 2nd of 8 (Quantitative) video tutorial. For more financial risk management videos, visit our website! http://www.bionicturtle.com

From playlist FRM

Jean-Pierre Florens: Inverse problems in econometrics - Lecture 1/4

Recording during the thematic month on statistics - Week 2 : "Mathematical statistics and inverse problems" the 9 February, 2016 at the Centre International de Rencontres Mathématiques (Marseille, France) Filmmaker: Guillaume Hennenfent Find this video and other talks given by worldwide

From playlist Probability and Statistics

Jean-Pierre Florens: Inverse problems in econometrics - Lecture 2/4

Recording during the thematic month on statistics - Week 2 : "Mathematical statistics and inverse problems" the 9 February, 2016 at the Centre International de Rencontres Mathématiques (Marseille, France) Filmmaker: Guillaume Hennenfent Find this video and other talks given by worldwide

From playlist Probability and Statistics

2012 FRM Quantitative Analysis T2.a

This is a sample of our 2012 FRM Quantitative Analysis T2.a video tutorials. View our products here: https://www.bionicturtle.com/products/financial-risk-management/ The Bionic Turtle program is the most effective and affordable preparation aid for the Financial Risk Manager (FRM) exam.

From playlist FRM

Statistics Lecture 3.4 Part 2: Finding the Z-Score. Percentiles and Quartiles

From playlist Statistics Playlist 1

Jean-Pierre Florens: Inverse problems in econometrics - Lecture 4/4

Recording during the thematic month on statistics - Week 2 : "Mathematical statistics and inverse problems" the 10 February, 2016 at the Centre International de Rencontres Mathématiques (Marseille, France) Filmmaker: Guillaume Hennenfent Find this video and other talks given by worldwide

From playlist Probability and Statistics

Data Science - Part XVI - Fourier Analysis

For downloadable versions of these lectures, please go to the following link: http://www.slideshare.net/DerekKane/presentations https://github.com/DerekKane/YouTube-Tutorials This lecture provides an overview of the Fourier Analysis and the Fourier Transform as applied in Machine Learnin

From playlist Data Science

Statistics Lecture 5.2: A Study of Probability Distributions, Mean, and Standard Deviation

https://www.patreon.com/ProfessorLeonard Statistics Lecture 5.2: A Study of Probability Distributions, Mean, and Standard Deviation

From playlist Statistics (Full Length Videos)

Threshold Switching Models | Switching Models in Econometrics, Part 2

This is the second video in a two-part series that shows how to model time series data in the presence of regime shifts in MATLAB in this video, we use Threshold Switching Models from the Econometrics Toolbox to model inflation data across different inflationary regimes. Download the code

From playlist Switching Models in Econometrics

Markov Switching Models | Switching Models in Econometrics, Part 1

This is the first video in a two-part series that shows how to model time series data in the presence of regime shifts in MATLAB. In this video, William Mueller uses Markov switching models from the Econometrics Toolbox to model unemployment data across different economic regimes. Downloa

From playlist Switching Models in Econometrics

Strata 2012: Hal Varian, "Using Google Data for Short-term Economic Forecasting"

Google Insights for Search provides an index of search activity for millions of queries. These queries can sometimes help understand consumer behavior. Hal describes some of the issues that arise in trying to use this data for short-term economic forecasts and provide examples. Hal Varian

From playlist Strata SC 2012

Introduction to Econometrics Toolbox in MATLAB

Get a Free Trial: https://goo.gl/C2Y9A5 Get Pricing Info: https://goo.gl/kDvGHt Ready to Buy: https://goo.gl/vsIeA5 Create a predictive time-series model of a stock index. For more videos, visit http://www.mathworks.com/products/econometrics/examples.html

From playlist Computational Finance

Statistics Lecture 4.2 Part 4: Introduction to Probability

From playlist Statistics Playlist 1