How to find the number of standard deviations that it takes to represent all the data

👉 Learn how to find the variance and standard deviation of a set of data. The variance of a set of data is a measure of spread/variation which measures how far a set of numbers is spread out from their average value. The standard deviation of a set of data is a measure of spread/variation

From playlist Variance and Standard Deviation

This video is about the Mean Absolute Deviation "On Your Own" ANSWERS 1) Mean = 12, the sum of the distances is 34, so the MAD is 34/8 = 4.25. The data values differ from the mean by an average of 4.25. 2) The mean absolute deviation should decrease because the distance between the new

From playlist Statistical Measures

How to find the variance and standard deviation from a set of data

👉 Learn how to find the variance and standard deviation of a set of data. The variance of a set of data is a measure of spread/variation which measures how far a set of numbers is spread out from their average value. The standard deviation of a set of data is a measure of spread/variation

From playlist Variance and Standard Deviation

Learning how to find the variance and standard deviation from a set of data

👉 Learn how to find the variance and standard deviation of a set of data. The variance of a set of data is a measure of spread/variation which measures how far a set of numbers is spread out from their average value. The standard deviation of a set of data is a measure of spread/variation

From playlist Variance and Standard Deviation

Measuring Variation: Range and Standard Deviation

This lesson explains how to determine the range and standard deviation for a set of data. Site: http://mathispower4u.com

From playlist Statistics: Describing Data

Ex: Calculate the Sample Standard Deviation

This video explains how to calculator the sample standard deviation of a data set. http://mathispower4u.com

From playlist Statistics: Describing Data

Standard Deviation and Variance

Understanding and calculating standard deviation and variance

From playlist Unit 1: Descriptive Statistics

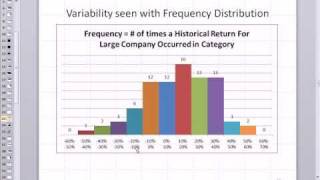

Level 1 Chartered Financial Analyst (CFA ®): Measures of dispersion including volatility

Session 2, Reading 8 (Part 2): A previous video in this CFA playlist looked at classic measures of central tendency. This is also called the first moment of the distribution or the distributions the location where is the distribution centered. When we say that I think most of us think of t

From playlist Level 1 Chartered Financial Analyst (CFA ®) Volume 1

Risk Management Lesson 4B: Volatility (second part) and Coherent Risk Measures

This is the second half of Lesson 4. Topics: - Exercise about volatility modeling with G-arch - Coherent risk measures - Are the variance and the standard deviation coherent? A useful document for you is available here: https://www.dropbox.com/s/6pdygf0bw6bcce1/coherence.pdf

From playlist Risk Management

Downside risk measures: semi-deviation, downside deviation, and Sortino ratio (FRM T1-12)

The two typical measures of downside risk focus on only the "bad" dispersion: Semi-deviation squares returns below the MEAN return, while downside deviation squares returns below a TARGET return (aka, minimum acceptable return, MAR). The Sortino Ratio divides by the downside deviation. [He

From playlist Risk Foundations (FRM Topic 1)

Excel Finance Class 98: Stock Return Variation Measured with Standard Deviation (Risk of Stock)

Download Excel File: https://people.highline.edu/mgirvin/YouTubeExcelIsFun/Busn233Ch10.xlsx Download PowerPoints: https://people.highline.edu/mgirvin/YouTubeExcelIsFun/Bsun233Ch10.pptx Learn about how to see and measure the volatility in Stock Returns using Standard Deviation. See how to

From playlist Excel Finance Free Course at YouTube. Cash Flow Analysis and Model Building (110 Videos).

Excel Finance Class 99: US Capital Market History 5 Types Investments (2 Good Lessons)

Download Excel File: https://people.highline.edu/mgirvin/YouTubeExcelIsFun/Busn233Ch10.xlsx Download PowerPoints: https://people.highline.edu/mgirvin/YouTubeExcelIsFun/Bsun233Ch10.pptx Learn about US Capital Market History 5 Types Investments. See that see can learn two good lessons: 1.

From playlist Excel Finance Free Course at YouTube. Cash Flow Analysis and Model Building (110 Videos).

Risk Management Lesson 1: Risk, Risk Management and the Efficient Frontier

First class of the Risk Management course I teach in the Minor Finance of TU Delft (2019/2020), The Netherlands. Contents: - risk management as a discipline - the aims of risk management - what is risk? - basic epistemology of risk - first tools: expected return, standard deviation - the

From playlist Risk Management

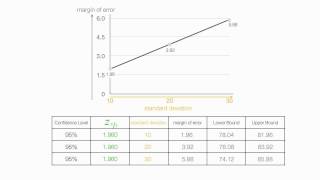

How to calculate margin of error and standard deviation

In this tutorial I show the relationship standard deviation and margin of error. I calculate margin of error and confidence intervals with different standard deviations. Playlist on Confidence Intervals http://www.youtube.com/course?list=EC36B51DB57E3A3E8E Like us on: http://www.facebook

From playlist Confidence Intervals

MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013 View the complete course: http://ocw.mit.edu/18-S096F13 Instructor: Kenneth Abbott This is an applications lecture on Value At Risk (VAR) models, and how financial institutions manage market risk. License: Creative

From playlist MIT 18.S096 Topics in Mathematics w Applications in Finance

Diversification in Investing: Response to Meet Kevin, Kevin O'Leary, Graham Stephan.

#KevinOLeary #GrahamStephan #Response #MeetKevin Today's video is a response to a viewer question about a comment financial YouTuber "Meet Kevin" made on diversification in his reaction to a video where Kevin O'Leary recommended that Graham Stephan diversify his investment portfolio. We wi

From playlist Statistics For Traders

FRM: Risk-adjusted performance ratios

RAPMs are variations of: return per unit of risk. Treynor and Sharpe are similar: both are excess return per unit of risk. Treynor defines risk as systematic risk (beta) and is therefore appropriate to well-diversified portfolios (i.e., into such portfolios idiosyncratic risk is eliminated

From playlist Performance measures

Prob & Stats - Random Variable & Prob Distribution (30 of 53) Standard Deviation

Visit http://ilectureonline.com for more math and science lectures! In this video I will explain the standard deviation of random variables. Next video in series: http://youtu.be/XiTMW8-aXXM

From playlist iLecturesOnline: Probability & Stats 2: Random Variable & Probability Distribution

Introduction to Confidence Intervals (Part 2)

This video introduces confidence intervals.

From playlist Confidence Intervals

Prof. Frank Riedel - Frank Knight, the Economics of Uncertainty, and 21st Century Finance

A workshop to commemorate the centenary of publication of Frank Knight’s "Risk, Uncertainty, and Profit" and John Maynard Keynes’ “A Treatise on Probability” This workshop is organised by the University of Oxford and supported by The Alan Turing Institute. For further details and regular

From playlist Uncertainty and Risk