FRM: Counterparty credit exposure

Study note: Counterparty credit risk is harder because (i) the initial value is 0 and the future value is highly uncertain and (ii) the contract can gain or lose. Two key metrics are Expected Exposure and Potential Future Exposure (PFE, which is essentially a VaR). For more financial risk

From playlist Credit Risk: Counterparty

How do you risk manage portfolios that contain financial derivatives?

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle Derivatives are specific types

From playlist Risk Management

FRM: Risk contribution of credit to portfolio unexpected loss

Risk contribution is analogous to systematic risk in single-factor (capital asset pricing model): as Ong says, it is a measure of the “undiversified risk of an asset in the portfolio. It is the amount of credit risk which cannot be diversified away by placing the asset in the portfolio.” F

From playlist Credit Risk: Introduction

What is a Credit Default Swap? | CDS | Credit Derivatives

In todays video we learn about Credit Default Swaps - Credit Derivatives. These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitte

From playlist Swaps

Low Default Portfolios (Part 1)

A Low Default Portfolio (LDP) is a portfolio characterized by a low number of defaults. Too simple? Citing the BCBS (Basel Committee on Banking Supervision): Several types of portfolios may have low numbers of defaults. For example, some portfolios historically have experienced low numb

From playlist Topics in Credit Risk Modelling

Liquidity support in a securitization

Internal liquidity support includes: Liability design (e.g., time tranching) or a Liquidity Reserve. External support includes: Lines of credit (LOC) and asset swaps

From playlist Credit Risk: Securitization

QRM L1-1: The Definition of Risk

Welcome to Quantitative Risk Management (QRM). In this first class, we define what risk if for us. We will discuss the basic characteristics of risk, underlining some important facts, like its subjectivity, and the impossibility of separating payoffs and probabilities. Understanding the d

From playlist Quantitative Risk Management

Risk Management Lesson 7A: LGD and Credit Ratings

In this first part of Lesson 7, we continue our discussion about credit risk, by analyzing the loss given default (LGD), and by introducing credit ratings as a simple way of dealing with the creditworthiness of a counterparty. This apparently simple knowledge is important to understand som

From playlist Risk Management

2012 FRM Credit Risk Measurement & Management T6.b

This is a sample of our 2012 FRM Credit Risk Measurement & Management T6.b video tutorials. You may view our products here: https://www.bionicturtle.com/products/financial-risk-management/ The Bionic Turtle program is the most effective and affordable preparation aid for the Financial Ri

From playlist FRM

A CLN is similar to a credit default swap (CDS): both transfer credit risk to investors. However, the CLN is FUNDED; the bond owner does not really incur counterparty risk. Instead, the investors (CLN Buyers) incur counterparty risk. Plus, they are concerned with correlation between the CL

From playlist Derivatives: Credit Derivatives

Synthetically Long Position with Credit Default Swap (CDS)

This illustrates how an investor takes a synthetically long position in a bond with a credit default swap (CDS). The CDS allows the investor to expose to a more pure form of credit risk

From playlist Derivatives: Credit Derivatives

Risk Management Lesson 6B: Intro Credit Risk, The Standardized Approach and the IRBs.

Second part of Lesson 6. Topics: - Credit Risk (CR) as portmanteau risk - Credit Risk in the Basel Framework - The Standardized approach to CR - The Basics of IRBs

From playlist Risk Management

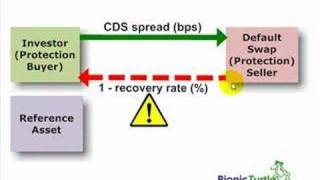

FRM: Credit default swap (CDS)

A CDS is a bilateral contract between two counterparties. The protection buyer is buying insurance: he/she pays premiums in exchange for a payoff in case there is a CREDIT EVENT (a trigger). For more financial risk videos, visit our website at http://www.bionicturtle.com!

From playlist Derivatives: Credit Derivatives

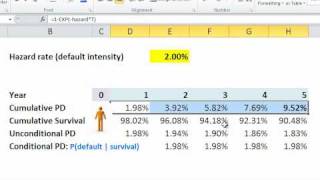

Conditional default probability (hazard rate)

Study note: Hazard rate (default intensity) is a conditional PD but it connotes an instantaneous rate of failure. As such, it can be used with elegance in the exponential distribution to compute the cumulative probability of default (cumulative PD). The conditional PD is the probability o

From playlist Credit Risk: Default

Risk Management Lesson 8B: Credit Default Swaps

In this second part of Lesson 8, we deal with CDS (Credit Default Swaps), understanding how they work, and how we can use them to quickly estimate the PD of a counterparty (under good market conditions).

From playlist Risk Management

Swaps and Credit Derivatives - Revision Lecture

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle

From playlist Revision Lectures

Unexpected loss (UL) of a portfolio of credit assets

The unexpected loss (UL) of a portfolio of credit assets incorporate individual asset ULs and pairwise default correlations

From playlist Credit Risk: Introduction

XVA desks in a post-Covid world: Brave new world or back to basics?

In 2020, when entire economies shut down, risk managers’ radars instantly picked up on the heightened financial risks. The same turbulence in the market also added new dimensions to the XVA desk – an already complex mission with regulatory, business, and technological elements to consider.

From playlist Webinars: At home with the experts