Fixed income: Effective Convexity (FRM T4-37)

Effective convexity approximates modified convexity (just as effective duration approximates modified duration). Mathematically, convexity is a function of the bond's second derivative with respect to yield: convexity = 1/P*∂^2P/∂y^2. Convexity is illustrated by the curvature (i.e., non-li

From playlist Valuation and RIsk Models (FRM Topic 4)

Convexity and The Principle of Duality

A gentle and visual introduction to the topic of Convex Optimization (part 2/3). In this video, we give the definition of convex sets, convex functions, and convex optimization problems. We also present a beautiful and extremely useful notion in convexity optimization, which is the princ

From playlist Convex Optimization

V3-32. Linear Programming. Convexity. Intersection of convex sets.

Math 484: Linear Programming. Convexity. Intersection of convex sets. Wen Shen, 2020, Penn State University

From playlist Math484 Linear Programming Short Videos, summer 2020

What is the difference between convex and concave

👉 Learn about polygons and how to classify them. A polygon is a plane shape bounded by a finite chain of straight lines. A polygon can be concave or convex and it can also be regular or irregular. A concave polygon is a polygon in which at least one of its interior angles is greater than 1

From playlist Classify Polygons

Just as (Macaulay) duration is weighted average maturity of bond, convexity is weighted average of maturity-squares of a bond (where weights are PV of bond cash flows). Dollar convexity is also the second derivative (d^2P/dy^2); i.e., the rate of change of dollar duration. Note: the corre

From playlist Bonds: Sensitivities

Lecture 7 | Convex Optimization I

Professor Stephen Boyd, of the Stanford University Electrical Engineering department, expands upon his previous lectures on convex optimization problems for the course, Convex Optimization I (EE 364A). Convex Optimization I concentrates on recognizing and solving convex optimization pro

From playlist Lecture Collection | Convex Optimization

Lecture 17 | Convex Optimization II (Stanford)

Lecture by Professor Stephen Boyd for Convex Optimization II (EE 364B) in the Stanford Electrical Engineering department. Professor Boyd lectures on Stochastic Model Predictive Control, he then begins discussing Branch-and-bound methods. This course introduces topics such as subgradient

From playlist Lecture Collection | Convex Optimization

Fixed Income: Duration and Convexity Summary (FRM T4-42)

In this playlist, I've already recorded at least ten videos on duration and convexity which are the two most common measures of single-factor interest rate risk. So, in this video, we wrap it up in one simple explanation that tries to illustrate both duration and convexity and how we apply

From playlist Valuation and RIsk Models (FRM Topic 4)

Fixed Income: Analytical Convexity; aka, modified convexity (FRM T4-41)

In this video, I will show you how to calculate modified convexity by matching the modified convexity that Tuckman shows in Table 4.6 in Chapter 4 of his book, Fixed Income Securities. 💡 Discuss this video here in our forum: https://trtl.bz/2YBEHeB. 📗 You can find Tuckman's Fixed Income

From playlist Valuation and RIsk Models (FRM Topic 4)

Your Dreams May Come True with MTP2 by Caroline Uhler

COLLOQUIUM YOUR DREAMS MAY COME TRUE WITH MTP2 SPEAKER: Caroline Uhler (Massachusetts Institute of Technology, Cambridge) DATE: Mon, 22 July 2019, 15:00 to 16:00 VENUE: Emmy Noether Seminar Room, ICTS Campus, Bangalore RESOURCES ABSTRACT We study probability distributions that are m

From playlist ICTS Colloquia

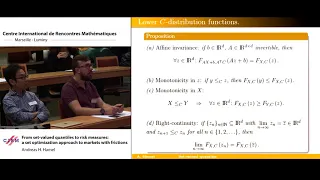

Andreas H. Hamel: From set-valued quantiles to risk measures: a set optimization approach to...

Abstract : Some questions in mathematics are not answered for quite some time, but just sidestepped. One of those questions is the following: What is the quantile of a multi-dimensional random variable? The "sidestepping" in this case produced so-called depth functions and depth regions, a

From playlist Probability and Statistics

The Adoption of Blockchain-Based Decentralized Exchanges (SIAM FME)

SIAM Activity Group on FME Virtual Talk Series Join us for a series of online talks on topics related to mathematical finance and engineering and running every two weeks until further notice. The series is organized by the SIAM Activity Group on Financial Mathematics and Engineering. Spea

From playlist SIAM Activity Group on FME Virtual Talk Series

How the portfolio possibilities curve (PPC) illustrates the benefit of diversification (FRM T1-7)

When correlations are imperfect, diversification benefits are possible. The portfolio possibilities curve illustrates this and it contains two notable points: the minimum variance portfolio (MVP) and the optimal portfolio (with the highest Sharpe ratio). At the end, I summarize four featur

From playlist Risk Foundations (FRM Topic 1)