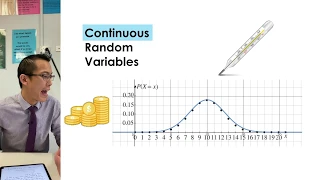

What are Continuous Random Variables? (1 of 3: Relation to discrete data)

More resources available at www.misterwootube.com

From playlist Random Variables

QRM L1-2: The dimensions of risk and friends

Welcome to Quantitative Risk Management (QRM). In this second video, we analyse the dimensions of risk. Risk is in fact an object that we need to consider from different points of view, and that sometimes we cannot even quantify. We will also discuss the importance of statistical thinking

From playlist Quantitative Risk Management

What are Continuous Random Variables? (2 of 3: Why we need different tools)

More resources available at www.misterwootube.com

From playlist Random Variables

Time Varying Volatility and GARCH in Risk Management

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle In Todays video let's learn abo

From playlist Risk Management

Expected shortfall: approximating continuous, with code (ES continous, FRM T5-03)

In my previous video, I showed you how we retrieve expected shortfall under the simplest possible discrete case. That was a simple historical simulation, but that was discrete. In this video, I'm going to review expected shortfall when the distribution is continuous. Specifically, I will u

From playlist Market Risk (FRM Topic 5)

Risk Management Lesson 4B: Volatility (second part) and Coherent Risk Measures

This is the second half of Lesson 4. Topics: - Exercise about volatility modeling with G-arch - Coherent risk measures - Are the variance and the standard deviation coherent? A useful document for you is available here: https://www.dropbox.com/s/6pdygf0bw6bcce1/coherence.pdf

From playlist Risk Management

Determine Continuous Random Variable Probabilities from Given Probabilities

This video explains how to determine probabilities of continuous random variables from given probabilities.

From playlist Continuous Random Variables

Stanford Webinar - Financing Innovation: Common Mistakes Even Great Investors Make

Innovation cannot happen without the funding to bring an idea to life. In this webinar Stanford Professor Peter DeMarzo, Senior Associate Dean of the Graduate School of Business and instructor within the Stanford Innovation and Entrepreneurship certificate, discusses how to value ideas and

From playlist Stanford Webinars

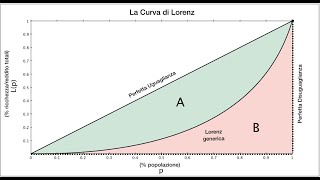

Fin Math L7: The Wang transform and the Lorenz curve in Black-Scholes-Merton

Welcome to Financial Mathematics. In this lesson we continue our discussion about the Wang transform and we also introduce an interesting connection with the Lorenz curve, a very useful instrument originally developed in the inequality studies' literature. As we shall see, the use of Wang

From playlist Financial Mathematics

In questo video parlo un po' dell'indice di Gini, importante misura di concentrazione utilizzata nello studio della disuguaglianza economica. Cerco di spiegare l'intuizione alla base dell'indice, e come evitare di farsi prendere per il naso, quando qualcuno ne parla. Indice: 00:00 Intro e

From playlist Sproloqui e commenti (in Italian)

Understanding Stock Market Basics | Wondrium Perspectives

S&P 500. NASDAQ. ETFs. If you listen to the news, these are terms you’ve heard many times. But if you are like many of us, you have no clue what the heck they mean. Now for some good news: In this episode of Perspectives, three financial experts give an easy-to-understand history of the

From playlist Wondrium Perspectives

Qualitative And Quantitative Risk Analysis Explained | Risk Analysis Techniques | Simplilearn

In this video on Qualitative and Quantitative Risk Analysis, we'll go into detail about how each of them work, how it's performed and the tools and techniques required to document it. 🔥Explore Our Free Courses With Completion Certificate by SkillUp: https://www.simplilearn.com/skillup-free

From playlist PMI-RMP® Training Videos [2022 Updated]

Quantitative Risk Analysis | What Is Quantitative Risk Analysis? | PMI-RMP Course | Simplilearn

This video on Quantitative Risk Analysis will help you understand how to perform Quantitative RIsk Analysis, List the tools and Techniques required for the analysis.This Video will also help you in EMV analysis and Probability Distribution. #QuantitativeRiskAnalysis #WhatIsQuantitativeRis

From playlist PMI-RMP® Training Videos [2022 Updated]

Qualitative Risk Analysis | What Is Qualitative Risk Analysis? | PMI-RMP Course | Simplilearn

This video will help you know how to perform Qualitative Risk Analysis. How to identify critical ridk factors and tools and techniques required to document the result of the Analysis. 🔥Free Project Management Course: https://www.simplilearn.com/learn-project-management-fundamentals-skillup

From playlist PMI-RMP® Training Videos [2022 Updated]

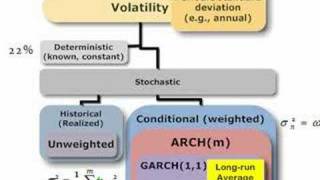

Lots of ways to estimate volatility. In this map, I parse out implied volatility (forward looking) and deterministic (constant) and focus on stochastic volatility: volatility that changes over time, either via (conditional) recent volatility and/or random shocks. For more financial risk vi

From playlist Volatility

Lecture 8: Risk-Sharing Application

MIT 14.04 Intermediate Microeconomic Theory, Fall 2020 Instructor: Prof. Robert Townsend View the complete course: https://ocw.mit.edu/courses/14-04-intermediate-microeconomic-theory-fall-2020/ YouTube Playlist: https://www.youtube.com/watch?v=XSTSfCs74bg&list=PLUl4u3cNGP63wnrKge9vllow3Y2

From playlist MIT 14.04 Intermediate Microeconomic Theory, Fall 2020

MIT 15.401 Finance Theory I, Fall 2008 View the complete course: http://ocw.mit.edu/15-401F08 Instructor: Andrew Lo License: Creative Commons BY-NC-SA More information at http://ocw.mit.edu/terms More courses at http://ocw.mit.edu

From playlist MIT 15.401 Finance Theory I, Fall 2008

What is Value at Risk? VaR and Risk Management

In todays video we learn about Value at Risk (VaR) and how is it calculated? Buy The Book Here: https://amzn.to/37HIdEB Follow Patrick on Twitter Here: https://twitter.com/PatrickEBoyle What Is Value at Risk (VaR)? Value at risk (VaR) is a calculation that aims to quantify the level of

From playlist Risk Management

Getting Started with Technical Analysis 2

⚠️ I have heard that YouTube might get rid of the comments section sometime next year. So that I can continue to answer your questions I created a Discord. I am available there basically all day to answer any questions you have about my videos. 🤗 MY DISCORD : https://discord.gg/2dkDmpVvgD

From playlist Technical Analysis