How to Use the Capital Asset Pricing Model (CAPM) to Value Investments

If you like this video, drop a comment, give it a thumbs up and consider subscribing here: https://www.youtube.com/c/HowToBeAnAdult?sub_confirmation=1 Read more on the Capital Asset Pricing Model and DOWNLOAD the FREE Excel file here: https://magnimetrics.com/capital-asset-pricing-model-c

From playlist Excel Tutorials

Pricing Options Using the Binomial Tree (Risk Neutral Valuation Approach)

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle In finance, the binomial option

From playlist Class 3: Pricing Financial Options

Capital asset pricing model (CAPM, FRM T1-9)

The CAPM is a ex ante single-factor model where the single-factor is the market's excess return: it says that we should expect an excess return that is proportional to the stock's beta, which is the stock's exposure to market's excess return, as measured by the stock's beta. Beta can be re

From playlist Risk Foundations (FRM Topic 1)

Dollar Cost Averaging - A Passive Stock Investment Strategy

This video tutorial provides a basic introduction into dollar cost averaging - a passive stock investment strategy that allows you to earn a decent return when a stock or a mutual fund is in an uptrend. This strategy neutralizes the effect of short term volatility and takes the guesswork

From playlist Stocks and Bonds

From playlist Courses and Series

Unit 5 - taxes efficiency part 1

From playlist Courses and Series

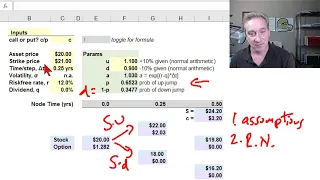

Introduction to binomial option pricing model: two-step (FRM T4-6)

[my xls is here https://trtl.bz/2AruFiH] The binomial option pricing model needs: 1. A set of assumptions similar but not identical to those found in Black-Scholes; 2. A framework; i.e., risk-neutral valuation which allows us to infer the probability of an up-jump; 3. An assumption about a

From playlist Valuation and RIsk Models (FRM Topic 4)

Unit 5 - practice problem 1 question

From playlist Courses and Series

Lecture 14: Real and Financial Flows: Thailand

MIT 14.04 Intermediate Microeconomic Theory, Fall 2020 Instructor: Prof. Robert Townsend View the complete course: https://ocw.mit.edu/courses/14-04-intermediate-microeconomic-theory-fall-2020/ YouTube Playlist: https://www.youtube.com/watch?v=XSTSfCs74bg&list=PLUl4u3cNGP63wnrKge9vllow3Y2

From playlist MIT 14.04 Intermediate Microeconomic Theory, Fall 2020

Paolo Guasoni, Lesson II - 19 december 2017

QUANTITATIVE FINANCE SEMINARS @ SNS PROF. PAOLO GUASONI TOPICS IN PORTFOLIO CHOICE

From playlist Quantitative Finance Seminar @ SNS

Theory of normal backwardation (FRM T3-17)

[here is my xls https://trtl.bz/2tBWdOY] If the commodity has positive beta, then the theoretical futures price is less than the expected future spot price: F(0) is less than E[S(t)]. Discuss this video here in our FRM forum: https://trtl.bz/2LP0Ctv.

From playlist Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

Lecture 4: Behavioral Development Economics: Introduction

MIT 14.771 Development Economics, Fall 2021 Instructor: Frank Schilbach View the complete course: https://ocw.mit.edu/courses/14-771-development-economics-fall-2021 YouTube Playlist: https://www.youtube.com/playlist?list=PLUl4u3cNGP61kvh3caDts2R6LmkYbmzaG Part 1 of 2 of Behavioral Deve

From playlist MIT 14.771 Development Economics, Fall 2021

Commodity cost of carry: Investment commodities (FRM T3-14)

[Here is my xls https://trtl.bz/2HoKR5d] The cost of carry model returns a theoretical forward price, which is based on the NET cost of ownership. Discuss this video here in our FRM forum: https://trtl.bz/2JJZi8M.

From playlist Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

Macroeconomic impacts of stranded fossil fuel assets - Mercure - Workshop 3 - CEB T3 2019

Mercure (University of Exeter) / 05.12.2019 Macroeconomic impacts of stranded fossil fuel assets ---------------------------------- Vous pouvez nous rejoindre sur les réseaux sociaux pour suivre nos actualités. Facebook : https://www.facebook.com/InstitutHenriPoincare/ Twitter :

From playlist 2019 - T3 - The Mathematics of Climate and the Environment

Discussion - Abrupt transitions and systemic risk by Amit Bhaduri and Srinivas Raghavendra

Modern Finance and Macroeconomics: A Multidisciplinary Approach URL: http://www.icts.res.in/program/memf2015 DESCRIPTION: The financial meltdown of 2008 in the US stock markets and the subsequent protracted recession in the Western economies have accentuated the need to understand the dy

From playlist Modern Finance and Macroeconomics: A Multidisciplinary Approach

Modern finance and Macroeconomics: connecting various threads by Srinivas Raghavendra

Modern Finance and Macroeconomics: A Multidisciplinary Approach URL: http://www.icts.res.in/program/memf2015 DESCRIPTION: The financial meltdown of 2008 in the US stock markets and the subsequent protracted recession in the Western economies have accentuated the need to understand the dy

From playlist Modern Finance and Macroeconomics: A Multidisciplinary Approach

MIT 14.04 Intermediate Microeconomic Theory, Fall 2020 Instructor: Prof. Robert Townsend View the complete course: https://ocw.mit.edu/courses/14-04-intermediate-microeconomic-theory-fall-2020/ YouTube Playlist: https://www.youtube.com/watch?v=XSTSfCs74bg&list=PLUl4u3cNGP63wnrKge9vllow3Y2

From playlist MIT 14.04 Intermediate Microeconomic Theory, Fall 2020

Unit 7 - no price discrimination part 1

From playlist Courses and Series

Gilles Pagès: CVaR hedging using quantization based stochastic approximation algorithm

Find this video and other talks given by worldwide mathematicians on CIRM's Audiovisual Mathematics Library: http://library.cirm-math.fr. And discover all its functionalities: - Chapter markers and keywords to watch the parts of your choice in the video - Videos enriched with abstracts, b

From playlist Analysis and its Applications