Effective Interest Rate (Effective Yield)

This video shows how to derive the effective interest rate formula for compounded and continuous interest. It also provides two examples on how to calculate effective interest rate. Site: http://mathispower4u.com Search: http://mathispower4u.wordpress.com

From playlist Finance: Simple and Compounded Interest

Effective Yield for Countinuous Interest

This video derives the effective yield formula and shows how to determine effective yield using the formula. http://mathispower4u.com

From playlist Finance: Simple and Compounded Interest

Unit 4 - practice problem 3 question

From playlist Courses and Series

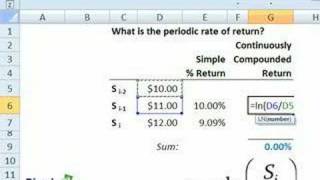

Intro to Quant Finance: Periodic Rate of Return

Periodic rate of return

From playlist Intro to Quant Finance

http://mathispower4u.wordpress.com/

From playlist Applications of Definite Integration

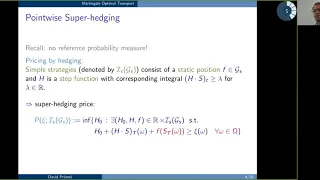

From playlist Contributed talks One World Symposium 2020

Dollar Cost Averaging - A Passive Stock Investment Strategy

This video tutorial provides a basic introduction into dollar cost averaging - a passive stock investment strategy that allows you to earn a decent return when a stock or a mutual fund is in an uptrend. This strategy neutralizes the effect of short term volatility and takes the guesswork

From playlist Stocks and Bonds

Unit 6 - price controls part 1

From playlist Courses and Series

Rails Conf 2013 Incremental Design - A conversation with a designer and a developer

By Rebecca Miller-Webster and Savannah Wolf Developers: how many times have you had to completely rip out your hard earned code for a totally new site design? Designers: how many times has a re-design taken 4 times as long as the developer said it would and not looked good in the end? Ch

From playlist Rails Conf 2013

Ninth SIAM Activity Group on FME Virtual Talk

Speaker: Sergey Nadtochiy, Associate Professor of Applied Mathematics, Illinois Institute of Technology Title: A simple microstructural explanation of the concavity of price impact Abstract: I will present a simple model of market microstructure which explains the concavity of price impa

From playlist SIAM Activity Group on FME Virtual Talk Series

Risk-Aware Reinforcement Learning for Finance (SIAM FME)

SIAM Activity Group on FME Virtual Talk Series Join us for a series of online talks on topics related to mathematical finance and engineering and running every two weeks until further notice. The series is organized by the SIAM Activity Group on Financial Mathematics and Engineering. Spe

From playlist SIAM Activity Group on FME Virtual Talk Series

Fifteenth SIAM Activity Group on FME Virtual Talk

Date: Thursday, December 10, 1PM-2PM Early Career Talks Speaker 1: Dena Firoozi, HEC Montréal - University of Montreal Title: Belief Estimation by Agents in Major-Minor LQG Mean Field Games Speaker 2: Sveinn Olafsson, Columbia University Title: Personalized Robo-Advising: Enhancing Inves

From playlist SIAM Activity Group on FME Virtual Talk Series

Time series analysis for Financial Data by A. S. Vasudeva Murthy

Program Summer Research Program on Dynamics of Complex Systems ORGANIZERS: Amit Apte, Soumitro Banerjee, Pranay Goel, Partha Guha, Neelima Gupte, Govindan Rangarajan and Somdatta Sinha DATE : 15 May 2019 to 12 July 2019 VENUE : Madhava hall for Summer School & Ramanujan hall f

From playlist Summer Research Program On Dynamics Of Complex Systems 2019

Thirteenth SIAM Activity Group on FME Virtual Talk

Speakers: Damir Filipovic, EPFL and Swiss Finance Institute Title: A Machine Learning Approach to Portfolio Pricing and Risk Management for High-Dimensional Problems Moderator: Rene Carmona, Princeton University

From playlist SIAM Activity Group on FME Virtual Talk Series

Boost Your Search with Apache Solr | Solr Search Engine Tutorial | Edureka

( Apache Solr Certification Training - https://www.edureka.co/apache-solr-self-paced ) Watch Sample Recording : http://www.edureka.co/apache-solr?utm_source=youtube&utm_medium=referral&utm_campaign=boost-search-solr Apache Solr based on the Lucene Library, is an open-source enterprise Gr

From playlist Apache Solr Tutorial Videos

RailsConf 2021: rails db:migrate:even_safer - Matt Duszynski

It's been a few years, your Rails app is wildly successful, and your database is bigger than ever. With that, comes new challenges when making schema changes. You have types to change, constraints to add, and data to migrate... and even an entire table that needs to be replaced. Let's lea

From playlist RailsConf 2021

Unit 7 - practice problem 4 question

From playlist Courses and Series